In this Edition:

GEOPOLITICAL RISK AND AI INVESTMENT SHAPE US MARKET DIRECTION

Higher oil prices briefly unsettled markets, but resilient economic data and renewed strength in AI-related shares helped support US equities as investors reassessed the interest-rate outlook.

EUROPE AND THE UK NAVIGATE ENERGY, INFLATION AND POLITICAL UNCERTAINTY

European inflation showed signs of moderating, although renewed energy-price risks and political change in the United Kingdom may influence fiscal policy, borrowing costs and investor confidence.

ASIAN MARKETS BALANCE TECHNOLOGY MOMENTUM WITH INFLATION PRESSURES

AI and semiconductor activity supported parts of the region, while persistent inflation in Japan and uneven domestic demand in China highlighted differing policy and consumer conditions.

GLOBAL ASSET PERFORMANCE REFLECTS A MORE SELECTIVE MARKET ENVIRONMENT

Equity returns diverged across regions as oil gained, bond yields moved higher in several developed markets and investors continued to distinguish between sectors and economies.

SOUTH AFRICA’S INFLATION OUTLOOK IMPROVES AS GROWTH REMAINS CONSTRAINED

A firmer rand and more contained oil-price assumptions have reduced immediate interest-rate pressure, but weak manufacturing activity and infrastructure constraints continue to weigh on the domestic economy.

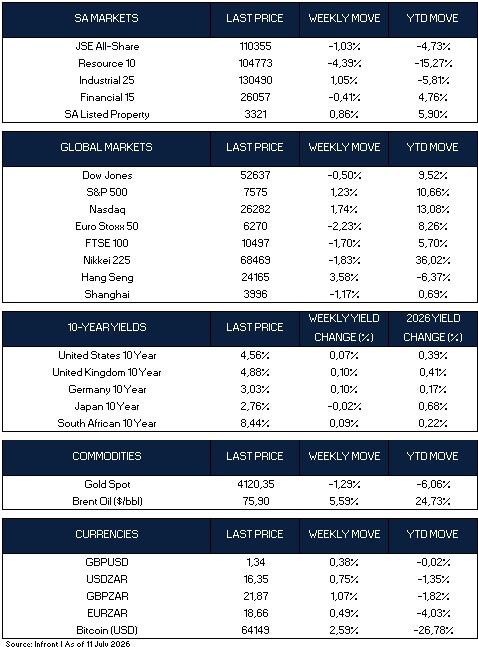

MARKET MOVES OF THE WEEK

Source: Infront (11 July 2026)

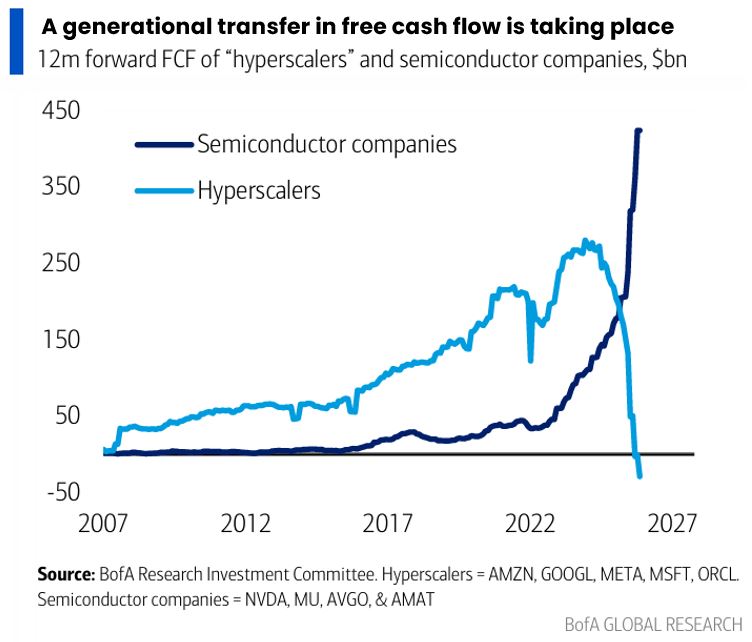

CHART OF THE WEEK

Source: BoFA Research Investment Committee (11 July 2026)

This chart from BofA Global Research illustrates a historic, generational transfer of free cash flow within the tech sector: the software giants are bleeding cash to fund the chip makers. To secure AI dominance, tech “hyperscalers” (AMZN, GOOGL, META, MSFT, ORCL) are burning through cash for infrastructure, plunging their collective 12-month forward free cash flow into negative territory. That massive tsunami of capital is pouring directly into semiconductor firms (NVDA, MU, AVGO, AMAT), fueling an unprecedented, parabolic surge in their cash flows. In short, the hyperscalers are bearing the immense strategic risk of the AI buildout, while the hardware layer captures all the immediate profit. (Source: BofA Research Investment Committee)

Geopolitical risk and AI investment shape US market direction

If investors needed a reminder that geopolitics and artificial intelligence remain two of the year’s dominant market drivers, the start of the third quarter provided one. Renewed hostilities between the United States and Iran pushed oil prices higher and briefly unsettled markets, but the equity market reaction was contained. Investors largely treated the escalation as a source of near-term headline risk, while renewed strength in semiconductor and AI shares helped the S&P 500 and Nasdaq recover from earlier weakness.

In the United States, minutes from the Federal Reserve’s June meeting showed that policymakers remain divided over the path for interest rates. A few officials saw a case for raising rates, although they ultimately supported leaving borrowing costs unchanged. Most also favoured removing language that implied an easing bias, reflecting uncertainty around persistent inflation, AI related demand and geopolitical risks.

Economic data remained broadly resilient. The ISM services index eased slightly to 54.0 in June but remained in expansion territory for a 24th consecutive month, while its employment component returned to growth. Initial jobless claims declined to 215,000 and continuing claims rose only modestly, suggesting that the labour market is cooling gradually rather than weakening sharply. Housing remained softer, with existing home sales falling by 2.4% as high prices and borrowing costs continued to constrain affordability.

Europe and the UK navigate energy, inflation and political uncertainty

In Europe, the renewed conflict between the United States and Iran raised concerns that higher energy prices could keep inflation and interest rates elevated. Germany offered some relief as annual inflation slowed to 2.3% in June from 2.6% in May. Other data were generally encouraging, with Dutch household consumption growing at its fastest pace in more than a year, German exports rising unexpectedly and Sweden recording a third consecutive month of economic growth while inflation eased slightly.

In the United Kingdom, politics took centre stage after Andy Burnham secured the support of 322 of Labour’s 403 Members of Parliament in the contest to replace Keir Starmer. Investors will be watching for clarity on his economic priorities, fiscal approach and cabinet appointments. The housing market remained subdued, with both new buyer enquiries and agreed sales still firmly negative as elevated mortgage costs continued to weigh on demand.

Asian markets balance technology momentum with inflation pressures

In Japan, the ten-year government bond yield ended the last week near 2.78%, despite briefly reaching its highest level since 1996. Yields later eased after Finance Minister Satsuki Katayama called on pension funds to increase allocations to domestic assets. Economic data continued to show persistent inflationary pressures, with wholesale prices rising by 7.1% year on year in June. Nominal wages increased by 3.2% in May, but real wage growth slowed to 1.4%, while household spending declined by a smaller-than-expected 0.4%, suggesting that consumer demand remained relatively resilient.

In China, AI and semiconductor developments supported technology shares early last week, although some gains were later reversed as investors took profits. Inflation data highlighted the divide between weak consumer demand and rising producer costs, with consumer inflation slowing to 1.0% in June while producer prices rose by 4.1%, the fastest pace in nearly four years. The People’s Bank of China maintained its supportive policy stance and pledged further assistance for domestic demand, technology investment and smaller businesses, but stopped short of announcing broad stimulus.

Global asset performance reflects a more selective market environment

Overall, global markets ended the last week on a mixed note. United States equities were broadly positive, with the S&P 500 gaining 1.23% and the Nasdaq rising by 1.74%, while the Dow Jones declined by 0.50%. European markets came under pressure, with the Euro Stoxx 50 and FTSE 100 falling by 2.23% and 1.70% respectively. Asian markets were mixed, as the Hang Seng gained 3.58%, while the Nikkei 225 and Shanghai Composite declined. Government bond yields rose across the United States, United Kingdom and Germany, while Japanese yields edged lower. In commodities, gold fell by 1.29%, while Brent crude oil rose by 5.59% and remains sharply higher year to date. Bitcoin gained 2.59% for last week but remains down by 26.78% in 2026.

South Africa’s inflation outlook improves as growth remains constrained

The outlook for South African interest rates became slightly more supportive after South African Reserve Bank Governor Lesetja Kganyago suggested that the inflationary impact of the Iran conflict may prove temporary, particularly if oil prices remain contained. This marked a softer tone than his comments a week earlier, when he focused more heavily on rising inflation expectations. The July Monetary Policy Committee meeting is therefore now more likely to leave interest rates unchanged rather than increase them by 0.25%, although the decision remains finely balanced.

The inflation outlook has also improved modestly, supported by lower oil prices and a firmer rand. Forecasts point to average inflation of around 3.9% in 2026 and 3.0% in 2027, with inflation potentially falling below 4% in the final quarter of this year. Should these trends continue, the Reserve Bank may be able to resume interest rate cuts in the first quarter of 2027, offering gradual support to household finances, bonds, listed property and other interest rate-sensitive assets.

The broader economy remains under pressure. Manufacturing production fell by 4.3% in the year to May, after declining by 2.9% in April, although monthly output improved by 1.1%. Producers continue to face high operating, infrastructure and fuel costs, as well as pressure from United States tariffs. South Africa’s net foreign exchange reserves also declined to $71.34 billion in June from $73.47 billion in May. The improving inflation outlook is encouraging, but weak industrial activity reinforces the need for faster reform and better infrastructure.

Against this backdrop, South African markets ended the last week weaker. The JSE All Share Index declined by 1.03%, with the sharpest pressure coming from resource shares, which fell by 4.39% and are now down by 15.27% year to date. Financials declined by 0.41%, while industrials and listed property were the relative bright spots, gaining 1.05% and 0.86% respectively. The rand weakened against major currencies, with the United States dollar ending the last week at R16.35, while the South African ten-year government bond yield rose to 8.44%.

The information contained in this recording/presentation is for general information purposes only and should not be construed as, nor does it constitute financial, tax, legal, investment or any other advice. Carrick does not guarantee the suitability or potential value of any products or investments discussed herein. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability or availability with respect to the information, products, services, or any other content contained in this recording for any purpose. Carrick accepts no responsibility for the suitability or accuracy of the information or for any errors or omissions that may occur. Therefore, any reliance you place on such information is strictly at your own risk. This material is provided for general information purposes only and is not personal advice to anyone to invest in any fund or product. Information taken from trade and other sources is believed to be reliable, although Carrick does not represent this as accurate or complete and it shouldn’t be relied upon as such. All material, content, and information provided by Carrick is the intellectual property of Carrick Group and its affiliates, unless otherwise stated. No part of this material may be copied, reproduced, distributed, published, or used for any commercial purpose without Carrick’s prior written consent, and is provided solely for non-commercial use. Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting an investment.