In this Edition:

LOWER OIL PRICES SUPPORT SENTIMENT, BUT INFLATION RISKS REMAIN

A temporary easing in Middle East tensions helped reduce oil-price pressure and improve market confidence, although central banks remain cautious about persistent inflation.

U.S. RESILIENCE KEEPS MARKETS CONSTRUCTIVE DESPITE CAUTIOUS FED MESSAGING

Technology-led gains and stronger consumer data supported U.S. equities, but the Federal Reserve’s unchanged stance signals that investors should remain measured on the timing of rate cuts.

EUROPE BENEFITS FROM ENERGY RELIEF WHILE GROWTH REMAINS UNEVEN

Lower oil prices and improved geopolitical conditions supported European sentiment, though weak regional growth and cautious policy expectations continue to shape the outlook.

JAPAN’S MARKET STRENGTH HIGHLIGHTS SHIFTING GLOBAL RATE DYNAMICS

Japan’s equity market momentum remains notable, but rising Japanese yields could have broader implications for global bond markets and international capital flows.

SOUTH AFRICA’S INFLATION OUTLOOK IMPROVES AS OIL PRICES EASE

A sustained fall in oil prices could reduce fuel-price pressure and support future policy flexibility, although food inflation and rand weakness remain important risks.

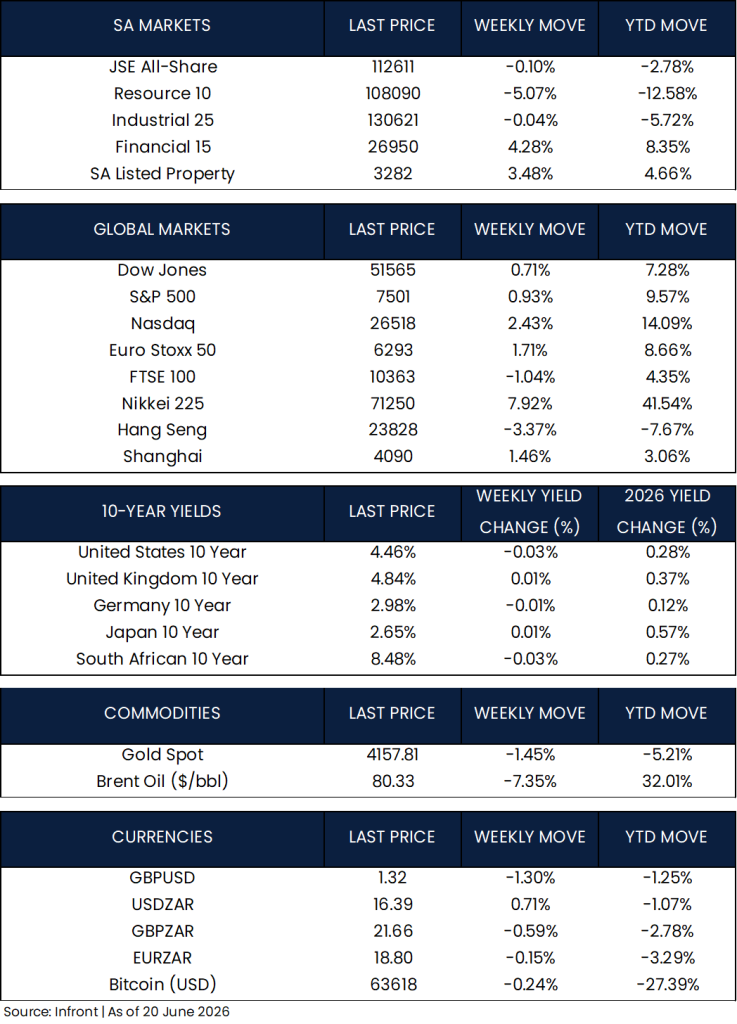

MARKET MOVES OF THE WEEK

Source: Infront (20 June 2026)

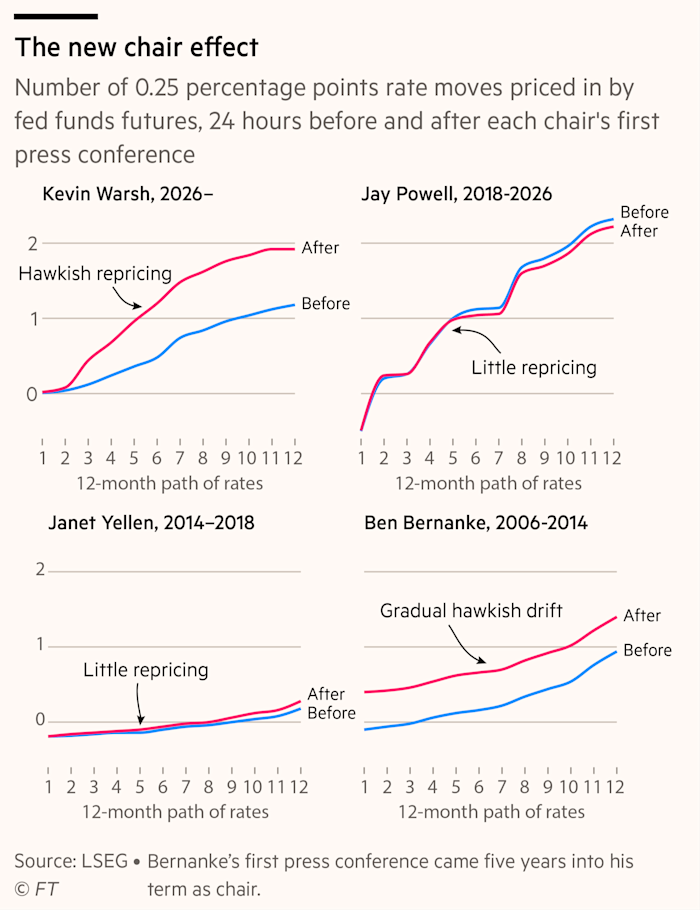

CHART OF THE WEEK

Source: Bloomberg (20 June 2026)

Markets sharply repriced the expected path of U.S. interest rates following Kevin Warsh’s first Federal Reserve press conference. Unlike previous Fed chair transitions, investors now expect significantly more tightening over the next 12 months, highlighting concerns that inflation may prove more persistent and that rates could remain higher for longer.

Lower oil prices support sentiment, but inflation risks remain

Global markets were broadly positive last week as investors welcomed signs of easing tensions in the Middle East. A temporary peace agreement between the United States and Iran helped reduce fears of a prolonged oil supply shock, with Brent crude falling 7.35% for the last week. Lower oil prices supported investor sentiment, although central banks remain alert to inflation risks.

U.S. resilience keeps markets constructive despite cautious Fed messaging

U.S. markets ended last week higher, led by technology shares. The Nasdaq rose 2.43%, the S&P 500 gained 0.93%, and the Dow Jones added 0.71%. Investor appetite for technology and artificial intelligence-related companies remained strong, while lower oil prices also helped improve market confidence.

The Federal Reserve left interest rates unchanged, but its message remained cautious. Policymakers are still concerned that inflation could stay higher for longer, especially after the recent jump in energy prices. This means investors should not assume that interest rate cuts are around the corner.

Economic data showed that the U.S. consumer remains resilient, with retail sales rising more than expected. However, the housing market remains under pressure as high borrowing costs continue to weigh on affordability. Overall, the U.S. economy still looks solid, but markets remain sensitive to any signs that inflation is not cooling quickly enough.

Europe benefits from energy relief while growth remains uneven

European markets also moved higher, supported by the improved geopolitical backdrop and lower energy prices. The Euro Stoxx 50 gained 1.71% for the last week, while the FTSE 100 declined 1.04%.

The Bank of England kept interest rates unchanged as it continues to balance inflation risks against a slower growth environment. Inflation has moderated, but policymakers remain cautious because energy prices can quickly feed through to household costs and business expenses.

In Europe, investor sentiment improved as confidence indicators in Germany recovered. However, economic data remains mixed, with parts of the region still facing weak growth. For now, lower oil prices are a welcome relief, especially for consumers and businesses that are sensitive to fuel and energy costs.

Japan’s market strength highlights shifting global rate dynamics

Asian markets were mixed last week. Japan was the clear standout, with the Nikkei 225 rising 7.92% and taking its year-to-date gain to 41.54%. Japanese shares were supported by continued enthusiasm around technology companies and the country’s exposure to global artificial intelligence investment.

At the same time, Japan remains an important market to watch from a global interest rate perspective. The Bank of Japan raised rates to their highest level since 1995 and continues to reduce bond purchases. This does not necessarily mean Japan is enjoying a simple growth boom. Rather, it reflects pressure from inflation risks, higher energy costs and a weak yen.

This shift matters because Japan has spent decades with extremely low interest rates. As Japanese yields rise, local investors may have more reason to keep money at home instead of investing overseas. Over time, this could have important implications for global bond markets, especially given Japan’s large role in funding international debt markets.

China’s market performance was more uneven. The Shanghai Composite gained 1.46%, while Hong Kong’s Hang Seng fell 3.37%. China’s industrial and export sectors remain relatively resilient, but consumer spending and property remain weak. Investors are still waiting for stronger evidence that policy support is feeding through into the broader economy.

South Africa’s inflation outlook improves as oil prices ease

South African markets were mixed. The JSE All Share Index slipped 0.10%, dragged lower by weakness in resources, which fell 5.07%. Financials were the strongest part of the local market, rising 4.28%, while listed property gained 3.48%.

The biggest local development was the potential change in the interest rate outlook following the temporary peace agreement between the United States and Iran. Brent crude fell sharply last week, which could ease pressure on South African fuel prices if the decline is sustained.

This matters because higher fuel prices had recently pushed inflation higher, rising from 3.1% in March to 4.5% in May. That increase contributed to the South African Reserve Bank raising interest rates at its May meeting. Deputy Governor Rashad Cassim indicated that if oil prices continue to fall and inflation pressure eases, it could make future policy decisions easier for the SARB.

However, South Africa is not completely out of the woods. Food prices remain a risk, especially if higher fertiliser costs or drought conditions place further pressure on the cost of living. The rand also remains important, as currency weakness can make imports more expensive and keep inflation elevated.

The information contained in this recording/presentation is for general information purposes only and should not be construed as, nor does it constitute financial, tax, legal, investment or any other advice. Carrick does not guarantee the suitability or potential value of any products or investments discussed herein. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability or availability with respect to the information, products, services, or any other content contained in this recording for any purpose. Carrick accepts no responsibility for the suitability or accuracy of the information or for any errors or omissions that may occur. Therefore, any reliance you place on such information is strictly at your own risk. This material is provided for general information purposes only and is not personal advice to anyone to invest in any fund or product. Information taken from trade and other sources is believed to be reliable, although Carrick does not represent this as accurate or complete and it shouldn’t be relied upon as such. All material, content, and information provided by Carrick is the intellectual property of Carrick Group and its affiliates, unless otherwise stated. No part of this material may be copied, reproduced, distributed, published, or used for any commercial purpose without Carrick’s prior written consent, and is provided solely for non-commercial use. Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting an investment.