Market Snapshot: AI-Led Gains as Oil Risks Ease

May delivered another positive month for global equities, although market leadership remained narrow and heavily concentrated in companies linked to artificial intelligence. After April’s strong rebound, investors continued to focus on resilient earnings and structural growth themes, while improving US-Iran negotiations toward month-end helped ease some pressure on energy markets.

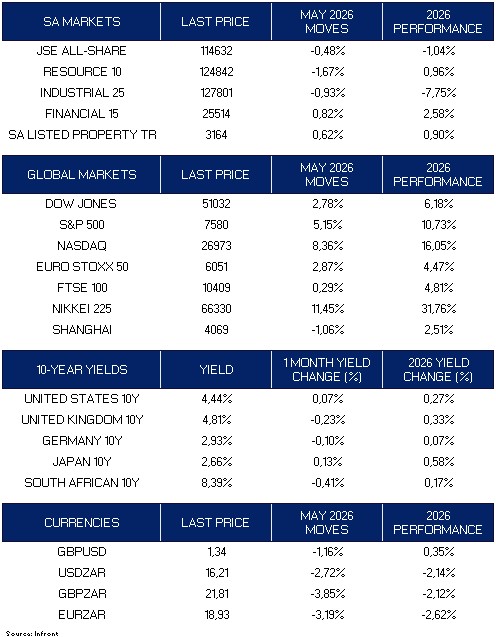

South African markets lagged global peers, with the FTSE/JSE All-Share declining 0.48% in May and ending the year-to-date period down 1.04%. Sector performance was mixed: financials (+0.82%) and listed property (+0.62%) gained, while resources (-1.67%) and industrials (-0.93%) declined. The local market’s limited exposure to the AI chipmaking companies that drove global and emerging market returns was a key reason for the relative underperformance.

Globally, equities delivered strong gains. The S&P 500 (+5.15%), Dow Jones (+2.78%) and Nasdaq (+8.36%) all moved higher, supported by strong earnings and continued momentum in technology shares. Japan (+11.45%) was the standout performer, while Europe also advanced, with the Euro Stoxx 50 (+2.87%) and FTSE 100 (+0.29%) higher. China was weaker, with the Shanghai Composite declining 1.06% as investors remained cautious about domestic demand and the strength of the recovery.

Bond markets remained volatile as investors weighed the inflation impact of higher oil prices against the possibility of geopolitical de-escalation. The US 10-year yield ended May at 4.44%, while South African yields declined to 8.39%, supporting local fixed income. Local assets were also helped by improved appetite for South Africa, attractive yields, a stronger rand and a more constructive view on the fiscal outlook.

Key Trends This Month:

- Global equities advanced, led by AI-related technology and semiconductor shares, although market leadership remained narrow.

- US earnings remained resilient, but inflation pressures and the change in Federal Reserve leadership kept interest-rate expectations in focus.

- Oil prices eased as US-Iran negotiations improved, although inflation risks remained elevated.

- South African equities lagged global peers, while the rand and local bonds were supported by the SARB’s 25bps rate hike, attractive yields and improved appetite for local assets.

Middle East Conflict: Oil Eases, Inflation Risks Remain

May delivered another positive month for global equities, although market leadership remained narrow and concentrated in companies linked to artificial intelligence. Investors focused on resilient earnings and structural growth themes, while improving US-Iran negotiations toward month-end helped ease pressure on energy markets.

South African markets lagged global peers, with the FTSE/JSE All-Share down 0.48% in May and 1.04% lower year-to-date. Sector performance was mixed: financials (+0.82%) and listed property (+0.62%) gained, while resources (-1.67%) and industrials (-0.93%) declined. The local market’s limited exposure to AI chipmakers, which drove global and emerging market returns, contributed to its underperformance.

Globally, equities advanced strongly. The S&P 500 (+5.15%), Dow Jones (+2.78%) and Nasdaq (+8.36%) all gained, supported by earnings and technology momentum. Japan (+11.45%) was the standout performer, Europe also advanced, and China weakened as concerns around domestic demand persisted.

Bond markets remained volatile as investors weighed oil-driven inflation risks against possible geopolitical de-escalation. The US 10-year yield ended May at 4.44%, while South African yields declined to 8.39%, supporting local fixed income. Local bonds and the rand were also helped by attractive yields and a more constructive fiscal outlook.

United States: AI and Earnings Lead Markets Higher

Equity Performance:

Dow Jones: +2.78%

S&P 500: +5.15%

Nasdaq: +8.36%

US equities delivered strong gains in May, supported by a resilient earnings season and renewed momentum in technology shares. The rally was particularly concentrated in AI-related areas, where demand for computing power, semiconductors and infrastructure remained a major driver of investor interest.

The macro backdrop was more mixed. Inflation remained elevated, with higher energy prices feeding into headline CPI, while producer prices also pointed to ongoing cost pressures. At the same time, labour market and retail sales data remained firm enough to reduce fears of a sharper slowdown.

Monetary policy also remained in focus after Kevin Warsh was sworn in as Federal Reserve Chair, with higher oil prices and inflation concerns pushing markets to price in a higher path for interest rates.

Outlook:

The US remains a key driver of global markets, but performance is increasingly concentrated in a narrow group of growth and AI-related companies. This supports returns in the near term but also increases concentration risk.

Europe and UK: Gains Despite Softer Data

Equity Performance:

Euro Stoxx 50: +2.87%

FTSE 100: +0.29%

European equities advanced during May, supported by stronger global sentiment and generally positive corporate earnings. However, performance lagged the strongest global markets, reflecting the region’s continued sensitivity to energy prices and weaker underlying economic momentum.

Eurozone growth forecasts were revised lower, while inflation expectations were revised higher. In the UK, weaker labour market data and lower-than-expected inflation helped gilts perform better, although political uncertainty added another layer of caution.

Outlook:

Europe continues to offer diversification, but performance remains closely linked to energy prices, growth expectations and central bank policy.

Japan: Strong Momentum Continues

Equity Performance:

Nikkei 225: +11.45%

Japan was one of the strongest-performing major markets in May. Equity gains were supported by technology and semiconductor shares, as investors continued to favour markets with exposure to the AI theme.

Japan’s first-quarter GDP also came in ahead of expectations, while softer inflation data reduced near-term pressure on the Bank of Japan to tighten policy. This combination of stronger growth data and reduced policy pressure supported investor sentiment.

Outlook:

Japan continues to benefit from global technology and AI demand, but remains sensitive to currency movements, energy prices and bond yield volatility.

China: Growth Concerns Persist

Equity Performance:

Shanghai Composite: -1.06%

Chinese equities delivered a weaker month, with investors remaining cautious about the domestic recovery. Services activity showed some resilience earlier in the month, but later data pointed to slower industrial production growth, weak retail sales and ongoing uncertainty around external demand.

Policy support remains important, but investors continue to question whether current measures will be enough to stabilise domestic momentum.

Outlook:

China remains a selective opportunity, with performance likely to depend on the strength of policy support and signs of improvement in domestic demand.

South Africa: Local Market Lags Global Peers

Equity Performance:

JSE All-Share: -0.48%

Resource 10: -1.67%

Industrial 25: -0.93%

Financial 15: +0.82%

SA Listed Property TR: +0.62%

South African equities ended May slightly lower, underperforming global and emerging market peers. Resources were weaker as gold’s recent tailwind faded, while industrials also declined. Financials and listed property performed better, supported by improved appetite for local assets and lower local bond yields.

The rand was a stronger point for local markets, supported by attractive yields, improved appetite for local assets and the South African Reserve Bank’s decision to raise rates by 25 basis points. The hike followed April inflation rising to 4.0% year-on-year and reflected the Bank’s intention to stay ahead of energy-driven price pressures.

Outlook:

South African assets continue to offer attractive yields, but equity performance remains heavily influenced by global drivers, commodity markets and currency movements.

Currencies: Rand Strengthens

Key Moves:

GBP/USD: -1.16% (1.34)

USD/ZAR: -2.72% (16.21)

GBP/ZAR: -3.85% (21.81)

EUR/ZAR: -3.19% (18.93)

Currency markets were supportive for South Africa during May. The rand strengthened against the dollar, pound and euro, helped by improved local sentiment, attractive yields and the SARB’s rate hike.

Takeaway:

Rand strength provided some support to local markets, although the currency remains sensitive to global risk appetite and commodity dynamics.

Fixed Income: Local Yields Move Lower

10-Year Yields (End-May | MoM change):

United States: 4.44% | +0.07%

United Kingdom: 4.81% | -0.23%

Germany: 2.93% | -0.10%

Japan: 2.66% | +0.13%

South Africa: 8.39% | -0.41%

Bond markets were volatile during May as inflation expectations shifted with oil prices and US-Iran negotiations. South African bonds performed well, with the local 10-year yield moving lower despite global inflation concerns.

Takeaway:

Fixed income remains sensitive to energy prices and central bank expectations, but easing inflation pressure could provide support if oil prices continue to normalise.

Final Thoughts: Markets Rise, But Gains Remain Concentrated

May reinforced the market’s willingness to look through geopolitical uncertainty when earnings are strong and structural growth themes remain powerful. Global equities delivered solid gains, but leadership was narrow and heavily concentrated in AI-related areas.

What this means for portfolios:

- Maintain diversification, as market leadership remains concentrated.

- Balance growth exposure with defensive assets, given ongoing inflation and geopolitical risks.

- Use global diversification to reduce reliance on any single region or sector.

While May was positive for global equities, the underlying environment remains complex. A diversified and disciplined approach remains important as markets continue to navigate narrow leadership, uncertain energy dynamics and cautious central banks.

Market Moves of the Month

The information contained in this recording/presentation is for general information purposes only and should not be construed as, nor does it constitute financial, tax, legal, investment or any other advice. Carrick does not guarantee the suitability or potential value of any products or investments discussed herein. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability or availability with respect to the information, products, services, or any other content contained in this recording for any purpose. Carrick accepts no responsibility for the suitability or accuracy of the information or for any errors or omissions that may occur. Therefore, any reliance you place on such information is strictly at your own risk. This material is provided for general information purposes only and is not personal advice to anyone to invest in any fund or product. Information taken from trade and other sources is believed to be reliable, although Carrick does not represent this as accurate or complete and it shouldn’t be relied upon as such. All material, content, and information provided by Carrick is the intellectual property of Carrick Group and its affiliates, unless otherwise stated. No part of this material may be copied, reproduced, distributed, published, or used for any commercial purpose without Carrick’s prior written consent, and is provided solely for non-commercial use. Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting an investment.