Risk-On Rally Defies Geopolitical Tension

April marked a sharp reversal from the risk-off environment of March, with global markets staging a powerful recovery despite continued geopolitical tension. While the conflict involving Iran and the ongoing disruption to energy supply remained a central macro driver, markets increasingly looked through these risks, supported by resilient corporate earnings and renewed investor appetite for growth assets.

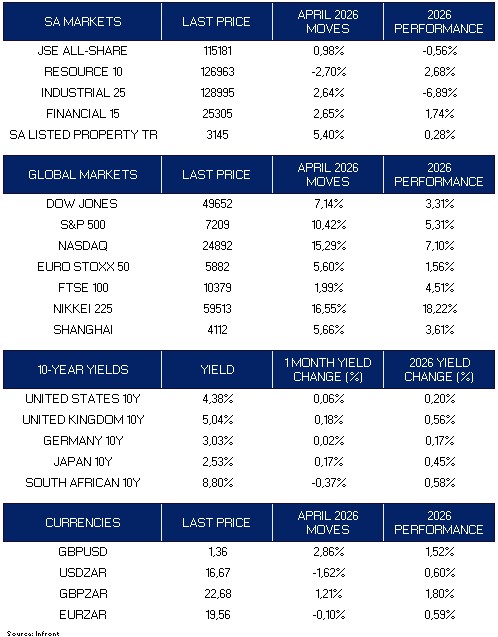

South African markets stabilised following March’s sharp sell-off. The FTSE/JSE All-Share rose 0.98%, recovering modestly but remaining slightly negative year-to-date (-0.56%). Performance was mixed across sectors, with financials (+2.65%) and industrials (+2.64%) leading the rebound. Listed property delivered a strong recovery (+5.40%), supported by declining local bond yields, while resources declined (-2.70%) amid continued commodity price volatility.

Globally, equity markets delivered strong gains across all major regions. The S&P 500 (+10.75%), Dow Jones (+6.81%) and Nasdaq (+16.32%) all moved sharply higher, with the latter reaching new highs driven by technology and AI-related stocks. Japan (+16.55%) was among the strongest performers, extending its year-to-date gains (+18.22%), while Europe (Euro Stoxx 50 +5.60%) and China (+5.66%) also participated in the rally.

Bond markets remained under pressure, although moves were more measured than in March. Yields edged higher across most developed markets, with the US 10-year rising to 4.38% (+0.06%) and the UK to 4.97% (+0.11%), reflecting persistent inflation concerns. In contrast, South African 10-year yields declined to 8.80% (-0.37%), providing some relief to local markets.

Currencies reflected improving sentiment. The US dollar softened modestly, while the rand strengthened, with USD/ZAR declining -1.81% to 16.64.

Key Trends in April

- Global equities rebounded strongly, led by technology and AI-driven growth sectors.

- Markets looked through geopolitical risks, focusing on earnings resilience and structural growth themes.

- Bond yields remained elevated, reflecting ongoing inflation concerns.

- The rand strengthened modestly as global risk appetite improved.

Middle East Conflict – Markets Balance Risk And Resilience

While April was characterised by a strong market recovery, the underlying geopolitical backdrop remained fragile. The conflict involving Iran continued to disrupt global energy supply, with the Strait of Hormuz remaining a key pressure point and oil prices elevated.

Despite this, markets increasingly shifted focus toward fundamentals:

- Corporate earnings proved resilient, particularly in the US and technology sectors.

- Investor positioning rotated back toward growth and long-term structural themes.

- Expectations of a prolonged inflation shock remained, but were partially offset by stronger economic data.

- Market volatility persisted, although price action became less reactive to headlines compared to March.

Importantly, markets are now balancing two competing narratives:

- A potential de-escalation scenario, which could ease energy prices and support further gains, and

- A prolonged disruption, which may sustain inflation pressures and challenge growth.

This dynamic continues to define the near-term outlook.

United States – Earnings and AI Drive Strong Recovery

Equity Performance:

- Dow Jones: +6.81%

- S&P 500: +10.75%

- Nasdaq: +16.32%

U.S. equities led the global recovery in April, supported by a strong earnings season and renewed momentum in technology stocks. The rally was particularly concentrated in AI-related sectors, which continue to benefit from strong investment and structural demand.

While higher energy prices and inflation remain concerns, economic data has remained broadly resilient. This has allowed markets to refocus on earnings growth rather than macro risks.

Outlook: The U.S. remains a key driver of global markets, with performance increasingly concentrated in growth sectors. While the backdrop remains constructive, markets are sensitive to inflation and policy expectations.

Europe – Recovery Despite Structural Headwinds

Equity Performance:

- Euro Stoxx 50: +5.60%

- FTSE 100: +1.84%

European markets recovered from March’s sharp declines, supported by improved global sentiment and resilient corporate earnings. However, performance lagged the US, reflecting the region’s continued sensitivity to energy prices and weaker underlying economic momentum.

The UK market delivered more modest gains, reflecting its defensive sector composition.

Outlook: Europe remains exposed to energy dynamics and slower growth. While valuations are supportive, performance is likely to remain linked to geopolitical developments and energy prices.

Japan – Strong Gains Continue

Equity Performance:

- Nikkei 225: +16.55%

Japan was one of the strongest-performing markets in April, extending its year-to-date gains. Performance was driven by strong exposure to global technology and AI-related demand, alongside improving investor sentiment.

However, the economy remains sensitive to energy prices given its reliance on imports.

Outlook: Japan continues to benefit from global growth themes but remains vulnerable to energy-related risks and currency dynamics.

China – Steady Recovery Continues

Equity Performance:

- Shanghai Composite: +5.66%

Chinese equities delivered solid gains, supported by policy stability and improving sentiment. While not a standout performer, the market continues to recover steadily following earlier weakness.

Domestic policy support and a more stable growth outlook have helped underpin performance.

Outlook: China remains relatively stable, but still dependent on global demand and ongoing policy support.

South Africa – Stabilisation After Sharp Sell-Off

Equity Performance:

- JSE All-Share: +0.98%

- Resource 10: -2.70%

- Industrial 25: +2.64%

- Financial 15: +2.65%

- SA Listed Property: +5.40%

South African markets stabilised in April following March’s sharp decline. The recovery was led by financials, industrials and listed property, supported by improved sentiment and lower bond yields.

Resources remained under pressure, reflecting ongoing commodity price volatility and uncertainty around global growth.

Outlook: South Africa remains supported by attractive valuations and high real yields, but performance continues to be driven by global factors, particularly currency movements and commodity prices.

Currencies – Rand Recovers Modestly

Key Moves:

- GBP/USD: +2.62% (1.36)

- USD/ZAR: -1.81% (16.64)

- GBP/ZAR: +0.70% (22.57)

- EUR/ZAR: -0.35% (19.51)

Currency markets reflected improving risk sentiment, with the US dollar weakening slightly and emerging market currencies recovering. The rand strengthened modestly against the dollar, although it remains sensitive to global developments.

Takeaway: Currency stability provided some support to local markets, although volatility is likely to persist.

Fixed Income – Yields Stabilise At Elevated Levels

10-Year Yields (End-April | MoM change):

- United States: 4.38% | +0.06%

- United Kingdom: 4.97% | +0.11%

- Germany: 3.03% | +0.03%

- Japan: 2.51% | +0.15%

- South Africa: 8.80% | -0.37%

Bond markets stabilised in April following March’s sharp repricing, although yields remain elevated. Inflation concerns, particularly linked to energy prices, continue to influence policy expectations.

The decline in South African yields provided support to local rate-sensitive sectors.

Takeaway: While pressure on bonds has eased, the broader environment remains challenging as inflation risks persist.

Final Thoughts – A Recovery, But Not Without Risk

April demonstrates how quickly market sentiment can shift. Despite ongoing geopolitical tension and elevated oil prices, markets have rebounded strongly, driven by earnings resilience and renewed confidence in growth sectors.

What this means for portfolios:

- Expect continued volatility as geopolitical risks remain unresolved.

- Market leadership is increasingly concentrated in growth and technology sectors.

- Diversification remains critical as correlations remain unstable.

- Local markets offer value, but remain highly dependent on global drivers.

While April’s recovery is encouraging, the underlying environment remains complex. Maintaining a disciplined and diversified approach remains key as markets continue to navigate a challenging macro backdrop.

Market Moves of the Month

The information contained in this recording/presentation is for general information purposes only and should not be construed as, nor does it constitute financial, tax, legal, investment or any other advice. Carrick does not guarantee the suitability or potential value of any products or investments discussed herein. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability or availability with respect to the information, products, services, or any other content contained in this recording for any purpose. Carrick accepts no responsibility for the suitability or accuracy of the information or for any errors or omissions that may occur. Therefore, any reliance you place on such information is strictly at your own risk. This material is provided for general information purposes only and is not personal advice to anyone to invest in any fund or product. Information taken from trade and other sources is believed to be reliable, although Carrick does not represent this as accurate or complete and it shouldn’t be relied upon as such. All material, content, and information provided by Carrick is the intellectual property of Carrick Group and its affiliates, unless otherwise stated. No part of this material may be copied, reproduced, distributed, published, or used for any commercial purpose without Carrick’s prior written consent, and is provided solely for non-commercial use. Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting an investment.