In this Edition:

U.S. MARKETS CLIMB AS INFLATION RISKS BUILD

Strong data and AI-led gains supported equities, but sentiment weakened and inflation expectations rose.

EUROPE CONTRACTS WHILE UK GROWTH HOLDS FIRM

Eurozone activity weakened, while UK data improved despite rising costs and softer confidence.

JAPAN RALLIES AS CHINA STEADIES AND HONG KONG LAGS

Japanese equities gained on technology strength, while Chinese markets delivered mixed results.

SOUTH AFRICAN MARKETS WEAKEN AS OIL RISKS RISE

Inflation edged higher, while the JSE and rand came under pressure.

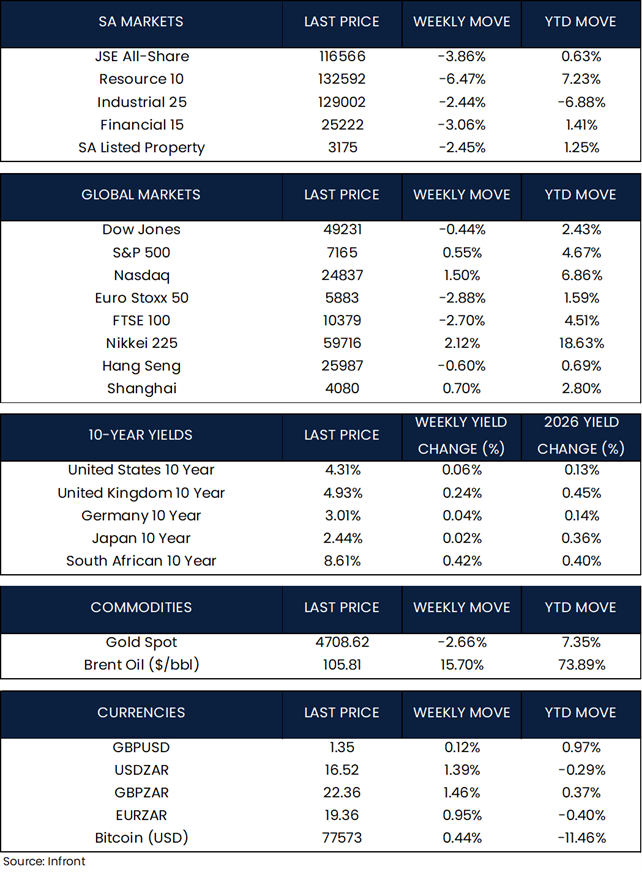

MARKET MOVES OF THE WEEK

Source: Infront (26 April 2026)

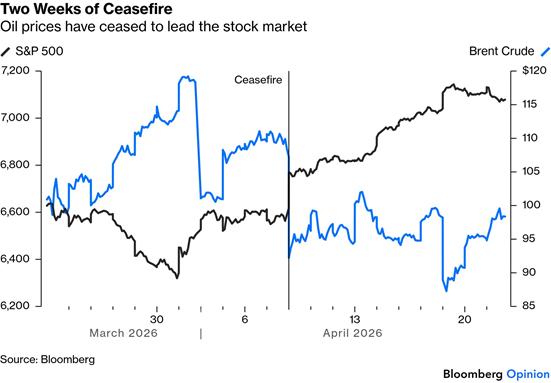

CHART OF THE WEEK

Source: Bloomberg (26 April 2026)

Crude oil prices surged, with Brent topping $100 for the first time in seven trading days. However, the usual inverse relationship between oil prices and U.S. equities has not held since the pause in hostilities three weeks ago. Despite ongoing disruptions, including the continued blockage of the Strait of Hormuz and stalled peace talks, the rise in crude coincided with gains in U.S. equities, highlighting the market’s resilience despite higher inflation risks.

U.S. markets climb as inflation risks build

U.S. economic data remained resilient in March, with retail sales rising 1.7%, the strongest monthly increase since early 2023. Gasoline station sales drove much of the gain, rising 15.5%, but underlying demand also held firm. Excluding gasoline stations, sales increased 0.6%, while control group sales, which feed directly into GDP, advanced 0.7%. Upward revisions to January and February data suggest that first-quarter activity was firmer than initially estimated.

U.S. business activity gained modest momentum in April after nearly stalling in March, although supply-side pressures intensified as factory delivery times lengthened, pushing output prices to a near four-year high. S&P Global’s flash U.S. Composite PMI rose to 52.0 from 50.3. Consumer sentiment, however, remained subdued. The University of Michigan Index of Consumer Sentiment declined by 3.5 points to 49.8, with weakness broad-based across demographics. Inflation expectations moved higher, with one-year expectations rising to 4.7% from 3.8% and long-term expectations increasing to 3.5%, the highest level since October 2025.

U.S. equities ended the week higher, with several indices reaching record highs as stronger economic data, AI-linked momentum, and supportive earnings helped offset geopolitical uncertainty. The technology-heavy Nasdaq Composite led gains, rising 1.50%, followed by the S&P 500, which advanced 0.55%. The Dow Jones Industrial Average, however, declined 0.44%. Oil prices surged 15.70% over the week to close at $105.81 per barrel, adding to inflation concerns.

Europe contracts while UK growth holds firm

Eurozone business activity contracted in April as geopolitical uncertainty weighed on demand and contributed to rising price pressures. S&P Global’s Flash Eurozone Composite PMI fell to 48.6 from 50.7, well below expectations and signalling contraction, while supply shortages continued to build, adding pressure to both growth and prices.

The UK provided a contrast to the weaker Eurozone picture, with business activity improving and retail sales exceeding expectations. The Composite PMI rose to 52.0 from 50.3, while UK retail sales increased 0.7% month-on-month in March, driven by fuel and non-food spending. However, input costs rose at the fastest pace on record, and consumer sentiment deteriorated, with the GfK Consumer Confidence Index falling to -25 in April, the lowest level since October 2023.

The pan-European STOXX Europe 50 Index ended last week down 2.88% in local currency terms, while the UK’s FTSE 100 declined 2.70%.

Japan rallies as China steadies and Hong Kong lags

Japan’s latest inflation data suggests that the impact of the Middle East conflict is beginning to filter through to the broader economy. Core CPI rose 1.8% year-on-year in March, ahead of expectations, driven by higher energy costs, although government subsidies provided some offset.

Separately, Xi Jinping called for an immediate ceasefire between the U.S. and Iran and the reopening of the Strait of Hormuz in a call with Mohammed bin Salman.

Asian equity performance was mixed. Japan’s Nikkei 225 gained 2.12%, extending its record highs, supported by strength in technology and AI-related stocks. Mainland Chinese equities were broadly stable, consolidating gains from the prior week’s stronger-than-expected economic data, with the Shanghai Composite Index edging up 0.70%. In contrast, Hong Kong equities underperformed, with the Hang Seng Index declining 0.60%.

South African markets weaken as oil risks rise

South Africa’s headline CPI rose to 3.1% year-on-year in March, up from 3.0% in February, according to Statistics South Africa. Price pressures broadened, with 6 of the 13 CPI categories recording higher annual inflation, including housing and utilities, transport, restaurants and accommodation, and education. The March print did not yet reflect the impact of higher oil prices linked to the Middle East conflict, which is expected to filter through in April.

Local equity markets declined over the last week as elevated geopolitical tensions and higher oil prices weighed on sentiment. The JSE All Share Index fell 3.86%, with broad-based weakness across sectors. Resources led the decline, falling 6.47%, followed by Financials (-3.06%), Industrials (-2.44%), and Listed Property (-2.45%). The rand ended the week 1.39% weaker against the U.S. dollar, closing at R16.52 on Friday.

The information contained in this recording/presentation is for general information purposes only and should not be construed as, nor does it constitute financial, tax, legal, investment or any other advice. Carrick does not guarantee the suitability or potential value of any products or investments discussed herein. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability or availability with respect to the information, products, services, or any other content contained in this recording for any purpose. Carrick accepts no responsibility for the suitability or accuracy of the information or for any errors or omissions that may occur. Therefore, any reliance you place on such information is strictly at your own risk. This material is provided for general information purposes only and is not personal advice to anyone to invest in any fund or product. Information taken from trade and other sources is believed to be reliable, although Carrick does not represent this as accurate or complete and it shouldn’t be relied upon as such. All material, content, and information provided by Carrick is the intellectual property of Carrick Group and its affiliates, unless otherwise stated. No part of this material may be copied, reproduced, distributed, published, or used for any commercial purpose without Carrick’s prior written consent, and is provided solely for non-commercial use. Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting an investment.