In this Edition:

CEASEFIRE OPTIMISM FUELS EQUITY RALLY DESPITE MIXED ECONOMIC SIGNALS

U.S. markets rallied strongly on easing geopolitical tensions and tech-led gains, even as inflation edged higher and consumer sentiment weakened.

GEOPOLITICAL RELIEF LIFTS MARKETS AMID A FRAGILE ECONOMIC BACKDROP

European equities rose on improved global sentiment, but underlying economic data and growth outlooks remain weak and uncertain

STRONG MARKET GAINS DRIVEN BY JAPAN’S SURGE AND IMPROVING SENTIMENT IN CHINA

Asian markets advanced, led by Japan’s sharp rally and supported by stabilising conditions in China despite ongoing consumer pressures.

GLOBAL TAILWINDS BOOST MARKETS WHILE RISING FUEL COSTS PRESSURE THE ECONOMY

South African markets benefited from improved global risk sentiment, though rising fuel costs and inflationary pressures pose risks to the local economy.

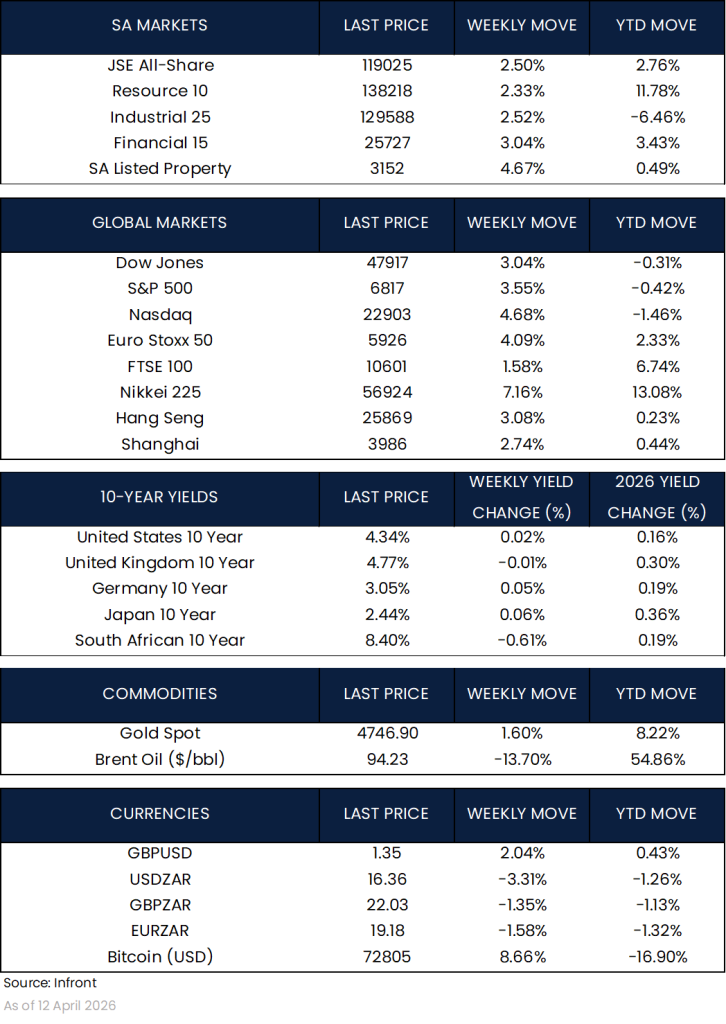

MARKET MOVES OF THE WEEK

Source: Infront (12 April 2026)

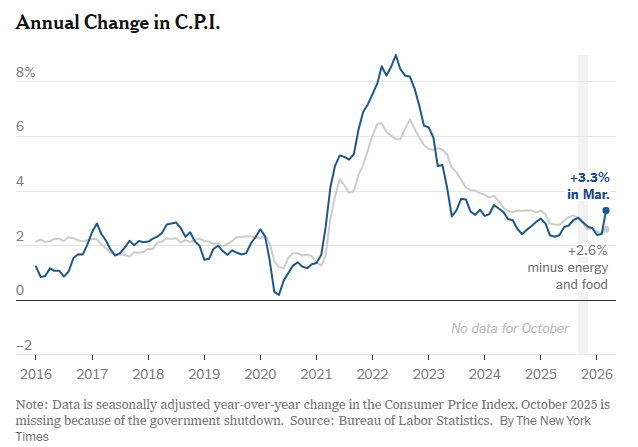

CHART OF THE WEEK

Source: U.S. Bureau of Labor Statistics, The New York Times (12 April 2026)

While markets rallied on easing geopolitical tensions, inflation remains elevated at 3.3%, with recent spikes in oil prices likely to keep upward pressure on headline numbers. This highlights the risk that energy-driven inflation may slow the pace of disinflation in the months ahead.

Ceasefire optimism fuels equity rally despite mixed economic signals

U.S. markets delivered another strong week of gains, marking a second consecutive week of positive performance. The S&P 500 rose 3.55%, the Dow Jones Industrial Average gained 3.04%, and the Nasdaq Composite led the way with a 4.68% increase.

Investor sentiment improved meaningfully as geopolitical tensions in the Middle East eased following news of a ceasefire agreement between the U.S. and Iran. This reduced concerns around oil supply disruptions and led to a sharp pullback in oil prices, which supported equity markets.

Technology stocks continued to drive performance, particularly those linked to artificial intelligence and semiconductors. Investors remain focused on long-term themes such as compute demand and infrastructure investment, which continue to underpin strong performance in this part of the market.

Economic data was more mixed. Inflation picked up slightly, largely due to higher energy prices, while consumer sentiment weakened. This suggests that while markets are responding positively to global developments, underlying pressure on consumers remains.

Geopolitical relief lifts markets amid fragile economic backdrop

European markets also moved higher during last week, supported by improving global sentiment. The Euro Stoxx 50 rose 4.09%, while the FTSE 100 gained 1.58%.

The rally was largely driven by easing geopolitical tensions, which encouraged investors to move back into equities. Gains were broad-based across the region, although performance varied between countries.

Despite the positive week for markets, the economic outlook remains uncertain. Policymakers have warned that growth forecasts may be revised lower, with risks of slower growth combined with rising inflation. This type of environment can be challenging for both businesses and consumers.

Recent data continues to reflect this mixed picture. Germany saw modest growth in factory orders, although below expectations, while services activity in France and Italy remained weak. In the UK, house price growth slowed, pointing to some pressure on the housing market.

While markets have responded positively to global developments, underlying economic conditions in the region remain somewhat fragile.

Strong market gains driven by Japan surge and improving sentiment in China

Asian markets delivered strong gains during the last week, supported by the improvement in global sentiment.

In Japan, the Nikkei 225 surged 7.16%, making it one of the best-performing major markets globally. The rally was led by technology and export-focused companies, which benefited from easing geopolitical tensions and improved global trade expectations.

A weaker yen continues to support exporters, although rising energy costs are beginning to feed into inflation. Consumer confidence declined during the last week, highlighting growing pressure on households.

In China, markets also moved higher. The Shanghai Composite Index rose 2.74%, while the Hang Seng Index gained 3.08%.

A notable development was the return of positive producer price inflation for the first time in several years, driven largely by higher commodity and energy prices. While this reflects rising cost pressures, it also suggests some stabilisation in industrial pricing.

Global tailwinds boost markets while rising fuel costs pressure economy

South African markets had a strong week, in line with the broader recovery across emerging markets. The FTSE/JSE All Share Index rose 2.50%, supported by improved global sentiment and renewed investor appetite for risk.

Performance was broad-based across sectors. Financials led the way, with the FTSE/JSE Financial 15 Index gaining 3.04%, while Industrials also performed well, with the FTSE/JSE Industrial 25 Index up 2.52%. Resources lagged slightly but still delivered positive returns, with the FTSE/JSE Resource 10 Index rising 2.33%. Listed property was a standout, posting a strong gain of 4.67%.

The rand strengthened during last week, with USD/ZAR falling 3.31%, supported by a weaker U.S. dollar and improving global risk sentiment.

While markets performed well, the local economic backdrop remains under pressure, particularly from rising fuel costs. Petrol prices have surged to a two-year high, while diesel has reached record levels.

These pressures are expected to feed through the broader economy. Transport costs are rising, which impacts the entire supply chain from raw agricultural inputs through to finished food products. As a result, consumers are likely to feel the effects through higher prices on everyday goods.

The government has attempted to cushion the impact by temporarily reducing fuel levies, providing some relief to households and businesses. However, South Africa remains particularly vulnerable to global energy shocks due to its reliance on imported fuel and fertiliser.

This creates an interesting dynamic. While global factors are currently supporting local markets, particularly through improved risk sentiment and capital flows, rising input costs present a near-term challenge for the domestic economy.

Overall, the last week highlights the dual nature of South Africa’s position. The market benefits quickly from improving global conditions, but the local economy remains sensitive to external shocks, particularly those linked to energy prices.

The information contained in this recording/presentation is for general information purposes only and should not be construed as, nor does it constitute financial, tax, legal, investment or any other advice. Carrick does not guarantee the suitability or potential value of any products or investments discussed herein. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability or availability with respect to the information, products, services, or any other content contained in this recording for any purpose. Carrick accepts no responsibility for the suitability or accuracy of the information or for any errors or omissions that may occur. Therefore, any reliance you place on such information is strictly at your own risk. This material is provided for general information purposes only and is not personal advice to anyone to invest in any fund or product. Information taken from trade and other sources is believed to be reliable, although Carrick does not represent this as accurate or complete and it shouldn’t be relied upon as such. All material, content, and information provided by Carrick is the intellectual property of Carrick Group and its affiliates, unless otherwise stated. No part of this material may be copied, reproduced, distributed, published, or used for any commercial purpose without Carrick’s prior written consent, and is provided solely for non-commercial use. Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting an investment.