Market Snapshot – Global Markets Diverge as Growth Moderates

February unfolded against a backdrop of moderating global growth, while inflation pressures continued to ease. Equity performance diverged more clearly across regions, with U.S. markets struggling during the month while Europe and Japan delivered stronger gains.

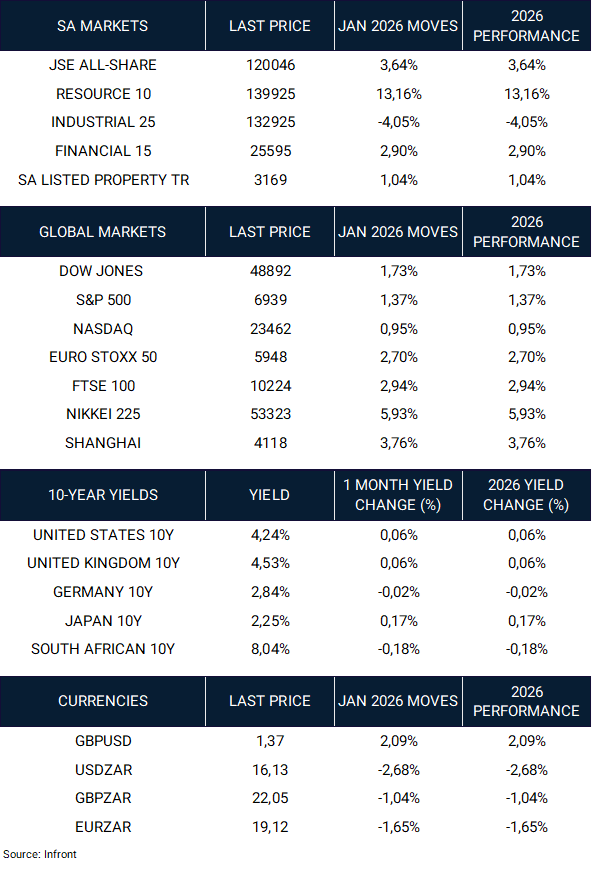

South African assets delivered a particularly strong performance. The FTSE/JSE All Share rose 7.01%, supported by a sharp rally in resources (Resource 10 +13.42%) and strong gains in financials (+7.42%). Industrials were broadly flat (-0.07%), while listed property advanced 6.29%, supported by declining bond yields. The rand also strengthened, with USD/ZAR falling 1.40% to 15.90, reinforcing supportive domestic financial conditions.

Globally, equity market performance diverged across regions. The Dow Jones (+0.17%) delivered modest gains, while the S&P 500 (-0.87%) and Nasdaq (-3.38%) declined, reflecting weakness in technology shares. By contrast, European equities delivered stronger gains, with the Euro Stoxx 50 rising 3.20% and the FTSE 100 gaining 6.72%, while Japan was a standout performer, with the Nikkei 225 surging 10.37%.

Toward the end of the month, renewed geopolitical tensions in the Middle East added a degree of uncertainty for markets, contributing to more cautious sentiment in the final trading days of February.

Key This Month:

- Global equity performance diverged, with weakness in U.S. technology shares contrasting with stronger gains in Europe and Japan.

- Bond yields declined across most markets, providing support for rate-sensitive assets such as listed property.

- South African equities delivered a strong month, led by a sharp rally in resource companies and solid gains in financials.

- The rand strengthened further against the U.S. dollar during the month as the dollar softened, reinforcing supportive domestic financial conditions.

United States – Technology Weakness Weighs on Markets

Equity Performance:

- Dow Jones: +0.17%

- S&P 500: -0.87%

- Nasdaq: -3.38%

U.S. equity markets delivered mixed performance during February, with weakness concentrated in technology shares. The Nasdaq declined 3.38% during the month, while the broader S&P 500 also finished lower.

Economic data released during the period pointed to moderating growth. U.S. GDP expanded at an annualised 1.4% in the fourth quarter, partly reflecting the impact of the government shutdown. At the same time, inflation continued to ease while labour market conditions remained relatively resilient. Consumer confidence also weakened during the period, highlighting growing concerns around the economic outlook.

Outlook: February’s pullback in U.S. technology shares highlights how quickly equity market leadership can shift. As performance becomes more differentiated across sectors and regions, broader participation will likely play a greater role in shaping market returns.

Europe – Stronger Month for Regional Equities

Equity Performance:

- Euro Stoxx 50: +3.20%

- FTSE 100: +6.72%

European equity markets delivered strong gains during February, outperforming U.S. benchmarks. Recent data across the region has pointed to moderating inflation pressures, while economic activity has remained mixed.

Against this backdrop, the FTSE 100 was a standout performer, rising 6.72% during the month, while the Euro Stoxx 50 advanced 3.20%. Performance in the U.K. market was supported in part by its greater exposure to banks and global resource companies, which performed strongly during the month. This contrasted with weaker performance in U.S. technology shares and contributed to the broader divergence in global equity returns.

Outlook: Europe continues to offer valuable diversification due to different sector composition and market drivers versus the U.S. Maintaining exposure helps reduce concentration risk and improves the resilience of global equity allocations.

Japan – Strong Market Performance Continues

Equity Performance:

- Nikkei 225: +10.37%

Japanese equities delivered one of the strongest performances among major markets during February, with the Nikkei 225 rising 10.37%.

Investor sentiment remained supportive, with Japanese equity indices reaching record highs toward the end of the month. Optimism around the domestic policy outlook and continued investor interest in Japanese markets helped support gains, while markets appeared largely unfazed by recent U.S. tariff announcements.

Outlook: Japan’s equity outlook continues to be supported by structural factors, including improving corporate governance reforms and the broader normalisation of the Japanese economy following decades of deflation. These developments are expected to support earnings growth and shareholder returns over time.

China – Modest Gains Amid Holiday-Shortened Month

Equity Performance:

- Shanghai Composite: +1.09%

- Hang Seng Index: -2.76%

Chinese mainland equities delivered modest gains during February, with the Shanghai Composite rising 1.09% during the month.

Trading activity across Chinese markets was somewhat muted during the period as investors observed the Lunar New Year holiday, which typically leads to reduced market activity across the region. Despite the quieter trading conditions, mainland equities still ended the month slightly higher.

Looking more broadly, the economic outlook for China remains mixed. The International Monetary Fund (IMF) expects China’s economy to expand by around 4–5% in 2026, reflecting continued policy support but also ongoing structural challenges within the economy.

Outlook: Market opportunities in China are likely to remain uneven as policymakers continue efforts to stabilise economic activity. As a result, a selective investment approach across sectors and themes remains important within global portfolios.

South Africa – Strong Returns with Broadening Sector Participation

Equity Performance:

- JSE All Share: +7.01%

- Resource 10: +13.42%

- Industrial 25: -0.07%

- Financial 15: +7.42%

- SA Listed Property TR: +6.29%

South African equities delivered a strong performance during February, with the FTSE/JSE All Share rising 7.01%. Resource companies were the primary driver of returns, surging 13.42% during the month, while financial shares also posted solid gains.

Industrials were broadly flat, reflecting the sector’s greater exposure to offshore earnings and global growth dynamics. Listed property delivered a strong return of 6.29%, supported by the decline in domestic bond yields during the month.

The macro backdrop was broadly supportive. Inflation remained contained, while the national budget was generally well received by markets as it reaffirmed the government’s commitment to fiscal discipline. Domestic bond yields declined during the month and the rand strengthened against the U.S. dollar.

Outlook: South African assets continue to offer attractive real yields within a global context. Encouragingly, market performance has also begun to broaden beyond resources, with other sectors presenting increasingly attractive opportunities for investors.

Currencies – Mixed Moves, Rand Strength Continues

Key Moves:

- GBP/USD: -1.48% (to 1.35)

- USD/ZAR: -1.40% (to 15.90)

- GBP/ZAR: -2.85% (to 21.42)

- EUR/ZAR: -1.69% (to 18.80)

Currency markets were mixed during February, with the U.S. dollar showing relative firmness against some developed market currencies. The South African rand strengthened against the dollar and also advanced against the euro and sterling, supported by favourable domestic conditions and improved sentiment toward emerging market assets.

Commodities – Mixed Performance

Commodity markets delivered mixed performance during February. Industrial metals and bulk commodities were broadly supported during the month, contributing to the strong performance of resource companies on the JSE. Toward the end of the month, geopolitical tensions between the United States and Iran briefly pushed oil prices higher as markets assessed the potential implications for global energy supply.

Fixed Income – Yields Decline Across Major Markets

10-Year Benchmark Yields (End-Feb | MoM change):

- US 10Y: 3.95% (-0.29%)

- UK 10Y: 4.23% (-0.30%)

- Germany 10Y: 2.65% (-0.19%)

- Japan 10Y: 2.11% (-0.14%)

- SA 10Y: 7.97% (-0.07%)

Government bond yields declined across most major markets during February as growth expectations moderated and inflation pressures continued to ease. South African bond yields also moved lower during the month. The decline in yields provided support for rate-sensitive assets, with listed property delivering a strong performance.

Final Thoughts – Diverging Markets Reinforce Diversification

February highlighted increasing divergence across global markets, with weaker U.S. technology performance contrasting with stronger gains in Europe and Japan. South African assets delivered a particularly strong month, supported by resource companies, a firmer rand and lower bond yields. Toward the end of the period, renewed geopolitical tensions also served as a reminder of the importance of diversification in navigating market uncertainty.

What this means for portfolios:

Broaden opportunity sets: market leadership is becoming more dispersed across regions and sectors, creating opportunities beyond traditional growth lead

Opportunities beyond resources: South African markets continue to present opportunities beyond the resource sector, with recent performance highlighting broader participation across sectors.

Maintain diversification across asset classes: Alternatives and real assets can help improve resilience during periods of geopolitical and macro uncertainty.

Market Moves of the Month

The information contained in this recording/presentation is for general information purposes only and should not be construed as, nor does it constitute financial, tax, legal, investment or any other advice. Carrick does not guarantee the suitability or potential value of any products or investments discussed herein. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability or availability with respect to the information, products, services, or any other content contained in this recording for any purpose. Carrick accepts no responsibility for the suitability or accuracy of the information or for any errors or omissions that may occur. Therefore, any reliance you place on such information is strictly at your own risk. This material is provided for general information purposes only and is not personal advice to anyone to invest in any fund or product. Information taken from trade and other sources is believed to be reliable, although Carrick does not represent this as accurate or complete and it shouldn’t be relied upon as such. All material, content, and information provided by Carrick is the intellectual property of Carrick Group and its affiliates, unless otherwise stated. No part of this material may be copied, reproduced, distributed, published, or used for any commercial purpose without Carrick’s prior written consent, and is provided solely for non-commercial use. Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting an investment.