In this Edition:

EARNINGS STRENGTH AND RESILIENT LABOUR DATA DRIVE US MARKET GAINS

Strong corporate earnings, resilient employment data and renewed AI optimism supported US equities despite weakening consumer confidence.

EUROPEAN MARKETS STEADY AS FIRMER DATA OFFSETS TARIFF CONCERNS

Improving factory activity and stronger business surveys supported European markets, although tariff risks and inflation pressures remained key concerns.

ASIAN EQUITIES ADVANCE AS JAPAN LEADS AND CHINA’S DEMAND STABILISES

Japanese technology shares and improving Chinese services activity lifted Asian markets, while investors remained cautious on trade uncertainty and domestic demand trends.

SOUTH AFRICA GAINS FISCAL CREDIBILITY AS GROWTH INDICATORS IMPROVE

Improving fiscal trends, stronger commodity-linked shares, and firmer business activity supported confidence in South African markets despite ongoing external risks.

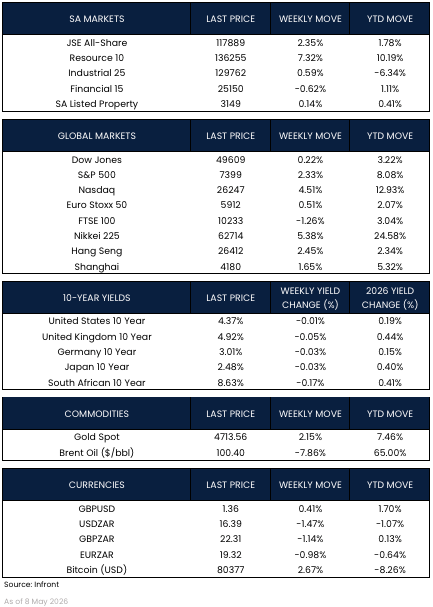

MARKET MOVES OF THE WEEK

Source: Infront (08 May 2026)

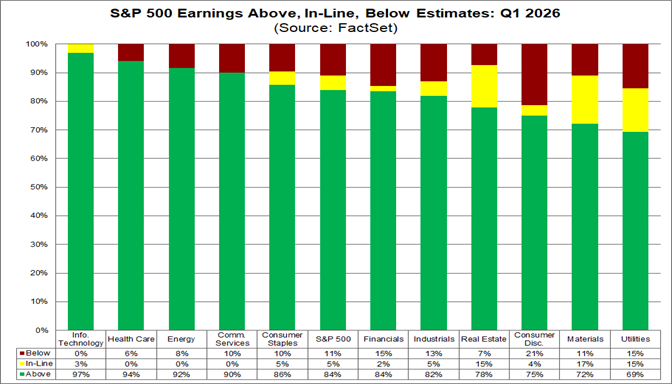

CHART OF THE WEEK

Source: FactSet (08 May 2026)

Q1 2026 has delivered one of the strongest U.S. earnings seasons in recent years, with 84% of S&P 500 companies beating earnings expectations. Information Technology has been the standout sector, with 97% of companies reporting earnings above analyst estimates.

Earnings strength and resilient labour data drive US market gains

U.S. equities advanced over the last week as investors took comfort from a resilient corporate earnings season and stronger-than-expected economic data. The S&P 500 gained 2.33%, while the Nasdaq rose 4.51%, reflecting renewed strength in technology and AI-related names. Earnings remained a key support for sentiment, with a large share of S&P 500 companies beating expectations and positive surprises particularly strong in aggregate. Information technology led the market higher, helped by continued optimism around AI infrastructure demand.

The U.S. labour market also remained firmer than expected. Initial jobless claims rose modestly but came in below consensus, while continuing claims declined to their lowest level since 2024. Nonfarm payrolls surprised positively, with April job gains exceeding expectations and March revised higher. This combination of resilient employment, solid earnings and firmer factory orders helped ease concerns that the U.S. economy was losing momentum too quickly.

However, the consumer picture was less encouraging. The University of Michigan consumer sentiment index fell sharply, with households increasingly concerned about higher gasoline prices and tariffs. For now, markets appear to be placing more weight on corporate earnings and labour resilience than on softer consumer confidence, but the divergence remains important to watch.

European markets steady as firmer data offsets tariff concerns

European markets were mixed but generally stable. The Euro Stoxx 50 gained 0.51%, while the FTSE 100 declined 1.26%. Sentiment improved earlier in last week on stronger corporate earnings and easing geopolitical concerns, but tariff uncertainty returned as a source of pressure after renewed U.S. threats toward the EU.

Economic data in Europe was somewhat firmer. German factory orders rose strongly in March, supported by broad-based demand across electrical equipment, data processing equipment and mechanical engineering goods. Eurozone producer prices also increased meaningfully, driven largely by energy prices, which could complicate the inflation outlook. In the UK, the composite PMI improved to 52.6, suggesting that business activity continued to expand, with both manufacturing output and services contributing to the improvement.

The key issue for investors remains the policy path. Any renewed pressure from energy prices or tariffs could make the inflation picture less comfortable, while weak growth still limits how aggressively central banks can tighten policy.

Asian equities advance as Japan leads and China’s demand stabilises

Asian markets were stronger over the last week. Japan was the standout performer, with the Nikkei 225 rising 5.38% in a holiday-shortened week. Gains were led by technology and semiconductor shares, supported by AI-related demand and lower oil prices, which helped reduce pressure on Japan’s import-heavy economy. The 10-year Japanese government bond yield eased slightly to 2.48%, while real wages rose for a third consecutive month, adding further evidence that Japan’s wage-price cycle is becoming more durable.

Chinese equities also advanced. The Shanghai Composite gained 1.65%, while the Hang Seng rose 2.45%. China’s services PMI improved to 52.6, pointing to resilient domestic demand, although export orders remained under pressure. Holiday travel data showed that domestic trips increased, but spending per trip softened slightly, suggesting that consumer activity is recovering, but still cautiously.

For China, the market remains focused on whether domestic demand can offset weaker external demand and ongoing trade uncertainty. Expectations of continued U.S.-China dialogue helped sentiment, but investors remain cautious given the limited likelihood of a major breakthrough.

South Africa gains fiscal credibility as growth indicators improve

South African markets were broadly positive, with the JSE All-Share gaining 2.35% and Resources rising 7.32%, supported by stronger commodity-linked shares. Financials declined 0.62%, while listed property was marginally positive. The rand strengthened against the dollar, with USDZAR moving down 1.47% over the last week, while the South African 10-year yield fell by 0.17%, indicating improved appetite for local assets.

The major local development was Moody’s more constructive view on South Africa’s fiscal outlook. Moody’s said South Africa’s improving fiscal performance and reform momentum should help stabilise government debt this year before it gradually declines. The agency currently rates South Africa at Ba2 with a stable outlook. It expects the general government deficit to narrow to 4.3% of GDP in 2026 and 3.8% in 2027, while debt is estimated to have peaked at 86.8% of GDP before easing gradually to 84.9% by 2028.

This is an important signal for local markets. Although South Africa’s debt burden remains high and interest costs still absorb a large share of revenue, the direction of travel appears to be improving. The combination of stronger revenue collection, spending restraint and reform progress has helped rebuild some fiscal credibility. That said, Moody’s also warned that external risks, including the Middle East conflict and its impact on growth and inflation, could still weigh on the outlook.

Domestic activity data was also encouraging. The S&P Global South Africa PMI rose to 51.6 in April from 50.8 in March, marking the fastest private-sector growth in 44 months. The improvement was driven by stronger sales, output and new orders, although firms continued to face cost pressures linked to a weaker rand, higher oil prices and freight disruptions.

The information contained in this recording/presentation is for general information purposes only and should not be construed as, nor does it constitute financial, tax, legal, investment or any other advice. Carrick does not guarantee the suitability or potential value of any products or investments discussed herein. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability or availability with respect to the information, products, services, or any other content contained in this recording for any purpose. Carrick accepts no responsibility for the suitability or accuracy of the information or for any errors or omissions that may occur. Therefore, any reliance you place on such information is strictly at your own risk. This material is provided for general information purposes only and is not personal advice to anyone to invest in any fund or product. Information taken from trade and other sources is believed to be reliable, although Carrick does not represent this as accurate or complete and it shouldn’t be relied upon as such. All material, content, and information provided by Carrick is the intellectual property of Carrick Group and its affiliates, unless otherwise stated. No part of this material may be copied, reproduced, distributed, published, or used for any commercial purpose without Carrick’s prior written consent, and is provided solely for non-commercial use. Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting an investment.