In this Edition:

ENERGY RISKS AND INFLATION PRESSURES KEEP GLOBAL MARKETS VOLATILE

Global markets remained cautious as rising oil prices and geopolitical tensions reignited inflation concerns.

US GROWTH SLOWS AS INFLATION PRESSURES REBUILD

The US economy showed slowing growth with renewed inflation risks, despite a still-resilient labour market.

EUROPE AND UK GROWTH SOFTENS UNDER ENERGY AND INFLATION STRAIN

Slowing activity and cautious consumers reflected the growing impact of energy costs and persistent inflation.

ASIA NAVIGATES ENERGY COSTS AND POLICY UNCERTAINTY

Japan and China faced mixed conditions as energy pressures and policy uncertainty shaped the regional outlook.

GLOBAL MARKETS MIXED AS INFLATION RISKS LIFT YIELDS

Equity markets were uneven while higher yields reflected ongoing inflation and geopolitical concerns.

SOUTH AFRICA SUPPORTED BY STABILITY BUT EXPOSED TO GLOBAL RISKS

Improved domestic conditions supported markets, though external risks, especially oil, remain a key concern.

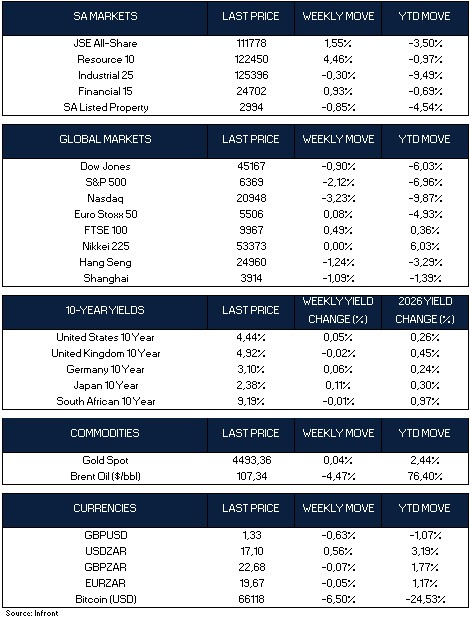

MARKET MOVES OF THE WEEK

Source: Infront (28 March 2026)

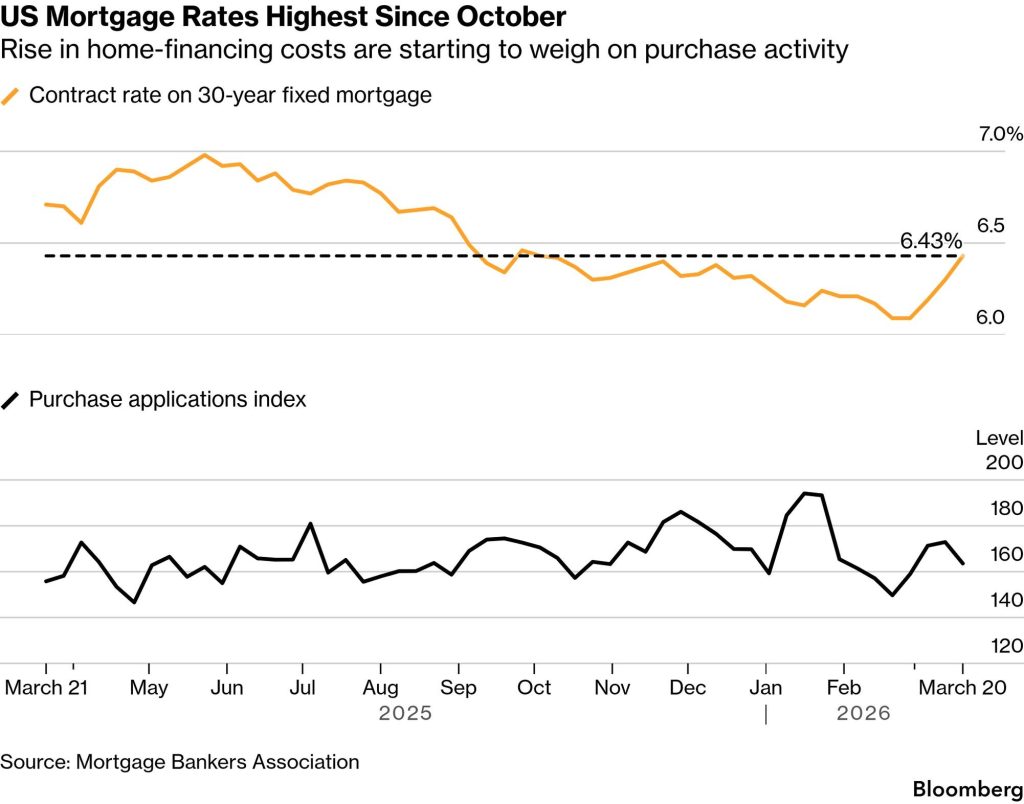

CHART OF THE WEEK

Source: Mortgage Bankers Association (28 March 2026)

Escalating tensions in the Gulf region and the associated surge in energy prices have driven a reassessment of the global interest rate outlook, with markets now pricing in rate increases across most major developed market central banks. Eight of the nine largest developed market central banks are expected to hike rates over the next 12 months, with the Federal Reserve the notable exception, where easing is still anticipated.

Energy Risks and Inflation Pressures Keep Global Markets Volatile

Global markets remained volatile last week. The conflict involving Iran continued to dominate sentiment, with markets reacting to every headline around ceasefire proposals, attacks on energy infrastructure and the prospects for a broader de-escalation. While hopes of diplomatic progress briefly improved sentiment early in the last week, those gains proved short-lived as the parties remain far apart in terms of any agreement. As a result, oil remained central to the market narrative, with investors increasingly concerned that a prolonged period of elevated energy prices could add to inflation pressures at a time when growth signals across major economies are already becoming more mixed.

Higher energy prices are already starting to feed through consumer and business expectations, complicating the outlook for central banks. If oil remains elevated for longer, policymakers may have less room to ease interest rates, even if economic momentum continues to soften. In the United States, for example, average gasoline prices have climbed to nearly $4 per gallon from around $2.80 at the start of the year, adding meaningful pressure to household budgets and reinforcing fears that higher energy costs could filter through into a broader range of goods and services.

US Growth Slows as Inflation Pressures Rebuild

In the United States, the economic backdrop remains mixed. Business activity is still expanding, but growth has slowed, with softer services activity offsetting some improvement in manufacturing. At the same time, pricing pressures have begun to pick up again, largely due to higher energy costs and supply chain disruptions linked to the Middle East conflict. This suggests that inflation risks may be re-emerging even as economic momentum moderates.

The labour market, however, continues to provide an important source of stability. Jobless claims remain relatively low and layoffs are still contained, indicating that businesses are not yet reacting aggressively to the more uncertain economic outlook. Even so, consumer sentiment weakened further in March as households grew more cautious about both the economic outlook and inflation. Against this backdrop, markets remained unsettled, with investors weighing two competing risks: slower growth on the one hand, and the possibility that the Federal Reserve may need to keep interest rates higher for longer if inflation proves more persistent.

Europe and UK Growth Softens Under Energy and Inflation Strain

In Europe and the UK, the economic backdrop is also becoming more fragile. Survey data pointed to slower growth in March, with eurozone business activity easing, German business confidence weakening and the OECD lowering its 2026 growth forecasts for both the eurozone and the UK. The common thread is that higher energy prices and geopolitical uncertainty are placing additional strain on economies that were already growing modestly.

At the same time, inflation remains sticky enough to limit how quickly central banks can respond. The European Central Bank has indicated that it stands ready to act, if necessary, but policymakers say it is still too early to judge whether the recent rise in energy prices will translate into a more persistent inflation problem. In the UK, headline inflation held around 3% in February, while softer retail sales, weaker consumer confidence and slowing services activity suggest that households are becoming more cautious again.

Asia Navigates Energy Costs and Policy Uncertainty

In Japan, higher oil prices and yen weakness remained central to the outlook. As a major energy importer, Japan is particularly exposed to rising oil costs, both through higher business input costs and pressure on household spending. At the same time, the yen’s weakness has kept the risk of official currency intervention in focus for investors. Although inflation softened somewhat in February, much of the decline reflected temporary government energy relief measures rather than a meaningful easing in underlying price pressures. As a result, the Bank of Japan is likely to proceed cautiously with any further policy normalisation.

China entered this period of geopolitical uncertainty with some tentative signs of improving momentum. Industrial profits rose strongly in the first two months of the year, and revenues also improved, suggesting that parts of the corporate sector began the year on a firmer footing. While these figures can be influenced by Lunar New Year timing effects, they nevertheless point to some stabilisation in business conditions, particularly among private firms where profit growth was notably stronger. Even so, China remains exposed to the broader global environment. Higher oil prices present a challenge for an economy that is a significant net importer of energy, prompting authorities to cap domestic fuel price increases to help cushion households and businesses. At the same time, trade tensions with the United States resurfaced, with Beijing initially striking a somewhat more conciliatory tone before later launching new investigations into US trade and supply chain practices.

Overall, last week reflected a mixed but generally cautious tone across global markets. In the United States, equities remained under pressure, with the Dow Jones down 0.90%, the S&P 500 declining 2.12%, and the Nasdaq falling 3.23%. European markets were more resilient, with the Euro Stoxx 50 edging up 0.08% and the FTSE 100 gaining 0.49%. In Asia, performance was mixed, as Japan’s Nikkei 225 was broadly unchanged last week, while Hong Kong’s Hang Seng fell 1.24% and China’s Shanghai Composite declined 1.09%. Bond yields moved modestly higher across most major developed markets as investors continued to weigh inflation risks and the interest rate outlook. In commodities, Brent crude oil fell 4.47% to $107.34 per barrel, although it remains sharply higher year to date, while gold was little changed last week and is up 2.44% for the year.

South Africa Supported by Stability but Exposed to Global Risks

In South Africa, the SARB left the repo rate on hold at 6.75%, in line with expectations, but the tone of the decision was slightly more reassuring than markets had anticipated. Governor Kganyago described the Bank’s approach as prudent, reflecting greater confidence in the recent improvement in South Africa’s macroeconomic backdrop. This was supported by subdued producer inflation, with PPI flat month on month in February and slowing to 1.8% year on year, reinforcing the view that underlying domestic price pressures remain relatively muted.

That said, the SARB also made it clear that the outlook remains vulnerable to external shocks, particularly through a weaker rand or a prolonged rise in oil prices. While the base case remains for rates to stay unchanged throughout the rest of the year, the Bank signalled that a more sustained energy shock could justify a 25-basis point hike as early as May. Elsewhere, there were modest signs of improvement in domestic sentiment, with the leading business cycle indicator rising in January and consumer confidence improving slightly in the first quarter, suggesting that lower rates, firmer asset prices and a steadier currency provide some support to the broader economy.

Against this backdrop, South African markets ended the last week firmer, diverging from the weaker tone seen across several major global equity markets. The JSE All Share Index gained 1.55%, supported primarily by a strong rebound in resource shares, while financials also posted a solid gain. Industrials were marginally weaker, and listed property softened modestly. Despite the weekly improvement, year-to-date performance remains mixed, with most major sectors still in negative territory. The rand softened modestly to R17.10 against the US dollar, while the South African 10-year government bond yield edged slightly lower to 9.19%.

The information contained in this recording/presentation is for general information purposes only and should not be construed as, nor does it constitute financial, tax, legal, investment or any other advice. Carrick does not guarantee the suitability or potential value of any products or investments discussed herein. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability or availability with respect to the information, products, services, or any other content contained in this recording for any purpose. Carrick accepts no responsibility for the suitability or accuracy of the information or for any errors or omissions that may occur. Therefore, any reliance you place on such information is strictly at your own risk. This material is provided for general information purposes only and is not personal advice to anyone to invest in any fund or product. Information taken from trade and other sources is believed to be reliable, although Carrick does not represent this as accurate or complete and it shouldn’t be relied upon as such. All material, content, and information provided by Carrick is the intellectual property of Carrick Group and its affiliates, unless otherwise stated. No part of this material may be copied, reproduced, distributed, published, or used for any commercial purpose without Carrick’s prior written consent, and is provided solely for non-commercial use. Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting an investment.