In this Edition:

HAWKISH FED STANCE AND ENERGY RISKS PRESSURE MARKETS

U.S. markets declined as persistent inflation, rising producer prices, and energy-driven geopolitical risks reinforced a more hawkish outlook for rates.

ENERGY SHOCK FEARS AND POLICY CAUTION WEIGH ON MARKETS

European markets fell as central banks flagged rising energy-driven inflation risks and ongoing geopolitical disruptions dampened sentiment.

POLICY DIVERGENCE AND ENERGY CONCERNS DRIVE CAUTIOUS SENTIMENT

Asian markets weakened as Japan signalled potential tightening amid energy risks, while China’s data pointed to only modest economic stabilisation.

SOFTER INFLATION OFFSET BY GLOBAL PRESSURES AND MARKET WEAKNESS

South African markets declined despite easing inflation, as higher oil prices and global risk-off sentiment weighed on equities and the rand.

MARKET MOVES OF THE WEEK

Source: Infront (22 March 2026)

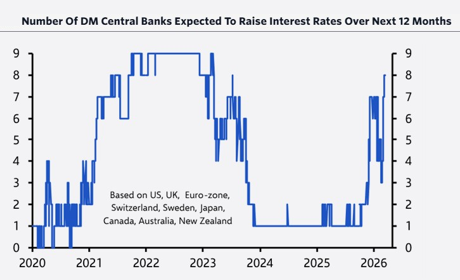

CHART OF THE WEEK

Source: LSEG, Capital Economics (22 March 2026)

Escalating tensions in the Gulf region and the associated surge in energy prices have driven a reassessment of the global interest rate outlook, with markets now pricing in rate increases across most major developed market central banks. Eight of the nine largest developed market central banks are expected to hike rates over the next 12 months, with the Federal Reserve the notable exception, where easing is still anticipated.

Hawkish Fed stance and energy risks pressure markets

The Federal Reserve left its federal funds target range unchanged at 3.50%–3.75% at its March policy meeting, marking a second consecutive hold. The decision was near-unanimous, with eleven members voting to maintain rates and one in favour of a cut. The updated Summary of Economic Projections retained a median expectation of one rate cut in 2026, while forecasts for both inflation and GDP growth were revised higher. In his post-meeting press conference, Chair Jerome Powell highlighted elevated uncertainty around the economic outlook, pointing to geopolitical developments in the Middle East and the risk of an energy shock as key risks to inflation expectations.

Inflation concerns were reinforced by the latest producer price data, with the Bureau of Labour Statistics reporting a 0.7% increase in February, up from 0.5% in January and the highest monthly reading since July 2025. On an annual basis, PPI rose to 3.4% from 2.9% with both measures exceeding consensus expectations.

U.S. equity markets ended last week lower amid a confluence of headwinds, including escalating geopolitical tensions, energy price volatility, persistent inflationary pressures, and a hawkish read of the Fed’s latest policy guidance. The Dow Jones Industrial Average was the weakest performer, falling 2.11% while the Nasdaq Composite shed 2.07% and the S&P 500 declined 1.90%. Gold and silver also declined as expectations for rate cuts eased, with markets shifting towards a more restrictive policy outlook. Brent crude surged 8.24% over last week to close at $112.36 per barrel.

Energy shock fears and policy caution weigh on markets

In Europe, the European Central Bank also held rates steady, with President Christine Lagarde noting that elevated oil and gas prices are expected to have a material impact on near-term inflation. The ECB revised its 2026 inflation forecast higher to 2.6% from 1.9% previously.

The Bank of England maintained its policy rate at 3.75%, in line with expectations, while cautioning that a sustained energy shock could prove inflationary and may require tighter policy. Separately, the Prudential Regulation Authority outlined proposals to strengthen liquidity buffers and enhance banking sector resilience during periods of market stress.

European equity markets declined over the last week, with sentiment weighed down by escalating Middle East tensions, including disruptions to energy infrastructure. The STOXX Europe 50 Index fell 3.77% in local currency terms, while the FTSE 100 declined 3.34%.

Policy divergence and energy concerns drive cautious sentiment

In Japan, the Bank of Japan held its policy rate at 0.75% as expected, although the decision was not unanimous, with one member voting for a hike. The policy statement emphasised the need to monitor geopolitical developments, global market volatility, and oil price dynamics. While inflation may temporarily dip below the 2% target, the BoJ expects higher energy costs to support a rebound in price pressures and reiterated that further rate increases remain possible.

China’s combined January and February activity data, published together to adjust for Lunar New Year distortions, came in modestly ahead of expectations, pointing to tentative stabilisation in economic momentum. Industrial production expanded 6.3% year on year, retail sales grew 2.8% and fixed asset investment grew 1.8% supported by infrastructure spend, which continued to offset weakness in the property sector. The data reduced the likelihood of near-term, large-scale policy stimulus.

In Asia, the Nikkei 225 declined by 0.83% in a holiday-shortened week. Chinese equity markets also moved lower, with sentiment weighed down by higher energy costs and ongoing concerns around subdued domestic demand. The Shanghai Composite fell 3.38% in local currency terms, while the Hang Seng Index was relatively more resilient, declining by 0.82%.

Softer inflation offset by global pressures and market weakness

South African inflation eased to 3.0% year on year in February 2026, down from 3.5% in January, largely due to base effects linked to a delay in medical aid adjustments. Housing and utilities were the main contributors, rising 4.8% and accounting for 1.1 percentage points of headline inflation. While the print came in softer, it is unlikely to shift the SARB’s near-term policy stance, with higher oil prices continuing to place upward pressure on inflation expectations.

Local equity markets retreated over the past week, mirroring weakness across global markets. The JSE All Share Index declined 4.22% weighed down primarily by a sharp drop in resources, which lost 9.99% over the last week. Industrials also ended lower, down 3.43% while financials held up relatively well, slipping just 0.07%. Property was the standout performer, gaining 2.03% and providing some relief to the broader index. The rand continued to soften against the U.S. dollar, closing at R17.00 on Friday.

The information contained in this recording/presentation is for general information purposes only and should not be construed as, nor does it constitute financial, tax, legal, investment or any other advice. Carrick does not guarantee the suitability or potential value of any products or investments discussed herein. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability or availability with respect to the information, products, services, or any other content contained in this recording for any purpose. Carrick accepts no responsibility for the suitability or accuracy of the information or for any errors or omissions that may occur. Therefore, any reliance you place on such information is strictly at your own risk. This material is provided for general information purposes only and is not personal advice to anyone to invest in any fund or product. Information taken from trade and other sources is believed to be reliable, although Carrick does not represent this as accurate or complete and it shouldn’t be relied upon as such. All material, content, and information provided by Carrick is the intellectual property of Carrick Group and its affiliates, unless otherwise stated. No part of this material may be copied, reproduced, distributed, published, or used for any commercial purpose without Carrick’s prior written consent, and is provided solely for non-commercial use. Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting an investment.