In this Edition:

Renewed Trade Tensions and Shutdown Weigh on Markets

Renewed trade tensions, a prolonged government shutdown and cautious Fed signals weighed on U.S. equities, while safe-haven demand lifted gold and lowered Treasury yields.

European Industrial Weakness and Political Uncertainty

Weak German industrial data and political instability in France pressured European markets, even as the ECB signalled inflation progress and gradual recovery expectations.

Japanese Equities Surge on Election Clarity as China Maintains Policy Support

Japanese stocks jumped on election certainty, while Chinese markets edged higher as policymakers reaffirmed a loose monetary stance.

Global Markets Mixed as Safe-Haven Demand Strengthens

Global equities delivered mixed returns as geopolitical uncertainty boosted gold and drove bond yields lower across major markets.

Policy Alignment Boosts Fiscal Confidence in South Africa

Clear alignment between fiscal and monetary authorities strengthened confidence in South Africa’s fiscal trajectory despite softer global risk sentiment.

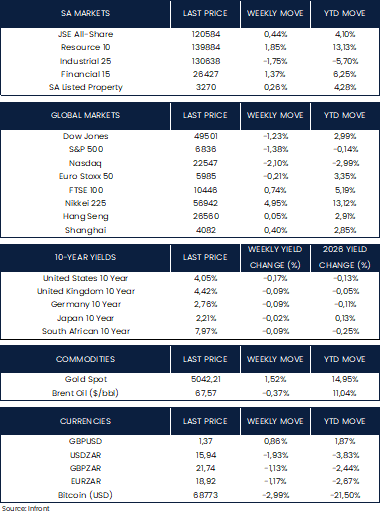

MARKET MOVES OF THE WEEK

Source: Infront (14 February 2026)

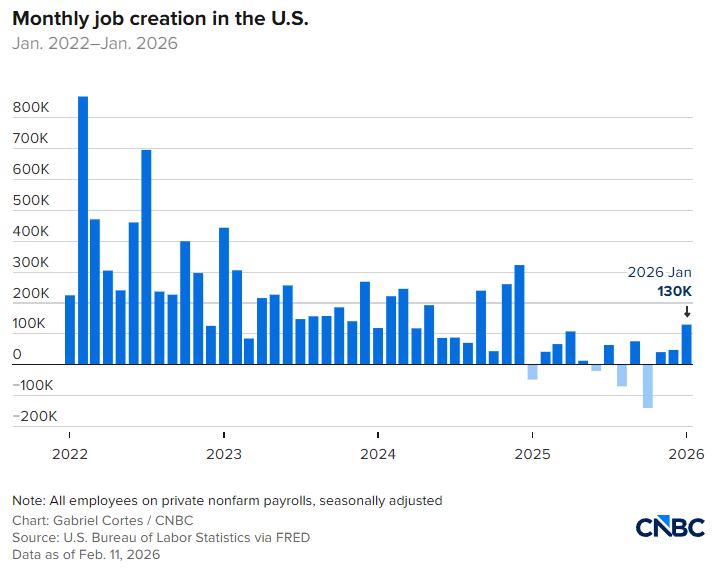

CHART OF THE WEEK

Source: U.S. Bureau of Labor Statistics via FRED (14 February 2026)

In January, U.S. nonfarm payrolls rose by 130,000, more than double the Dow Jones consensus estimate of 55,000, according to seasonally adjusted data from the Bureau of Labor Statistics released Wednesday. The report, which was delayed nearly a week due to the partial government shutdown that ended Feb. 3, shows a labour market still in a low-growth phase, with only isolated signs of rising layoffs. January marked the strongest month for job growth since December 2024, following a year in which monthly job gains averaged just 15,000.

Renewed Trade Tensions and Shutdown Weigh on Markets

Renewed trade tensions, a prolonged government shutdown and cautious Fed signals weighed on U.S. equities, while safe-haven demand lifted gold and lowered Treasury yields.

European Industrial Weakness and Political Uncertainty

Weak German industrial data and political instability in France pressured European markets, even as the ECB signalled inflation progress and gradual recovery expectations.

Japanese Equities Surge on Election Clarity as China Maintains Policy Support

Japanese stocks jumped on election certainty, while Chinese markets edged higher as policymakers reaffirmed a loose monetary stance.

Global Markets Mixed as Safe-Haven Demand Strengthens

Global equities delivered mixed returns as geopolitical uncertainty boosted gold and drove bond yields lower across major markets.

Policy Alignment Boosts Fiscal Confidence in South Africa

Clear alignment between fiscal and monetary authorities strengthened confidence in South Africa’s fiscal trajectory despite softer global risk sentiment.

Renewed Trade Tensions and Shutdown Weigh on Markets

The latest inflation data released in the U.S. by the Bureau of Labor Statistics showed further signs of easing price pressures in January. Headline consumer prices rose 0.2% month on month, down from 0.3% in December, while the annual inflation rate slowed to 2.4% from 2.7%, coming in below consensus expectations and marking the lowest level since May. The moderation was largely driven by a notable decline in energy prices, alongside favourable base effects as higher readings from a year ago dropped out of the annual calculation.

Core inflation, which excludes food and energy, increased 0.3% over the month, slightly firmer than December’s 0.2% reading and in line with forecasts. On an annual basis, core CPI rose 2.5%, matching expectations. While the headline data suggests that inflationary pressures are gradually easing, the steadier core reading indicates that underlying price dynamics remain somewhat sticky. Overall, the January report provides cautious optimism that inflation continues to trend in the right direction, even if progress remains uneven. This softer-than-expected inflation backdrop offered Wall Street a degree of relief during last week, strengthening expectations that the Federal Reserve could consider cutting interest rates later this year. Bond yields moved lower in response, with the US 10-year Treasury falling to 4.07% on Friday, its lowest level since early December, as the moderate CPI print reinforced the view that policy easing remains on the table even amid a resilient economy.

On Wednesday, the Bureau of Labor Statistics released January labour market data that exceeded expectations. Nonfarm payrolls rose by 130,000, well above consensus forecasts, while the unemployment rate ticked down to 4.3% from 4.4% in December. Job gains were led by healthcare, followed by social assistance and construction. The strong employment report highlights the continued resilience of the US economy, tempering expectations for aggressive interest rate cuts even as inflation shows signs of easing.

Equity markets, however, closed last week lower. The S&P 500 declined 1.39%, the Dow Jones Industrial Average fell 1.23%, and the Nasdaq Composite shed 2.1%, marking their largest weekly losses since November. Technology shares were particularly volatile, as concerns around artificial intelligence disruption and the significant capital expenditure required to support AI development weighed on sentiment.

European Industrial Weakness and Political Uncertainty

In Europe, the Euro STOXX 50 Index ended marginally lower as investors digested strong US jobs data and growing concerns about AI competition. Data from Eurostat showed that the eurozone economy expanded by 0.3% in the fourth quarter of 2025, offering modest support to the regional outlook.

In the UK, political uncertainty persisted amid calls for Prime Minister Keir Starmer to resign. Economic data from the Office for National Statistics indicated that real GDP grew by just 0.1% in Q4 2025, while annual growth reached 1%. Manufacturing activity improved over the quarter, though construction contracted. Retail sales rose 2.3% year on year in January, and the FTSE 100 added 0.74% over the last week.

Japanese Equities Surge on Election Clarity as China Maintains Policy Support

Japanese equities outperformed, with the Nikkei 225 surging 4.96% following the February 8 lower house election, where Prime Minister Sanae Takaichi’s Liberal Democratic Party secured a supermajority. In China, markets were modestly higher ahead of Lunar New Year holidays, with the Shanghai Composite Index gaining 0.43% while Hong Kong’s Hang Seng Index was little changed. The People’s Bank of China reiterated its commitment to a “moderately loose” monetary policy stance in 2026 as inflation data pointed to ongoing deflationary pressures.

Global Markets Mixed as Safe-Haven Demand Strengthens

In commodities, gold rebounded after recent weakness, supported by lower Treasury yields and a softer US dollar. Oil prices, however, edged lower, with Brent crude on track for a second consecutive weekly decline amid easing concerns over potential supply disruptions linked to US-Iran tensions.

Looking ahead, markets will focus on the Federal Reserve’s upcoming meeting minutes, US fourth-quarter GDP data, and income and spending figures. Canada’s inflation release, European PMIs, Japan’s GDP and inflation data, will also provide further insight into the global economic trajectory amid ongoing trade, fiscal, and monetary policy uncertainty.

Policy Alignment Boosts Fiscal Confidence in South Africa

On Thursday night, President Cyril Ramaphosa delivered a candid assessment of South Africa’s most urgent challenges, pledging decisive action on crime, water shortages, dysfunctional municipalities, and the next phase of Eskom’s restructuring. Crime took centre stage, with Ramaphosa describing organised criminal networks as “the most immediate threat to our democracy, our society and our economic development.” He announced a strengthened offensive, including the consolidation of intelligence at the national level and the deployment of multidisciplinary intervention teams aimed at dismantling criminal networks. The South African National Defence Force will also support police operations in hotspot areas.

On infrastructure, the government has committed over R156 billion to water and sanitation projects over the next three years, advancing initiatives such as the Lesotho Highlands Water Project and the Ntabelanga Dam. Municipalities that fail to deliver services, Ramaphosa warned, will face consequences. On the energy front, the first round of independent transmission projects will begin this year, enabling private investment to expand the grid, while work continues to address load-shedding caused by transformer overloading and illegal connections.

On the markets, the FTSE/JSE All Share Index ended last week modestly higher, up 0.44%, with mining and resource-linked stocks leading gains thanks to robust demand and favourable commodity prices. Financials also performed well, reflecting continued investor confidence in banks and lenders, while industrials lagged amid currency strength and softer sector performance.

On the currency front, the rand maintained a strong position below the 16.00 level against the dollar, buoyed by high precious metal prices (gold, platinum, palladium) and improved sentiment around South African economic reforms.

Looking ahead, market and economic attention will turn to South Africa’s fourth-quarter unemployment figures, January inflation data, and December retail sales numbers.

The information contained in this recording/presentation is for general information purposes only and should not be construed as, nor does it constitute financial, tax, legal, investment or any other advice. Carrick does not guarantee the suitability or potential value of any products or investments discussed herein. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability or availability with respect to the information, products, services, or any other content contained in this recording for any purpose. Carrick accepts no responsibility for the suitability or accuracy of the information or for any errors or omissions that may occur. Therefore, any reliance you place on such information is strictly at your own risk. This material is provided for general information purposes only and is not personal advice to anyone to invest in any fund or product. Information taken from trade and other sources is believed to be reliable, although Carrick does not represent this as accurate or complete and it shouldn’t be relied upon as such. All material, content, and information provided by Carrick is the intellectual property of Carrick Group and its affiliates, unless otherwise stated. No part of this material may be copied, reproduced, distributed, published, or used for any commercial purpose without Carrick’s prior written consent, and is provided solely for non-commercial use. Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting an investment.